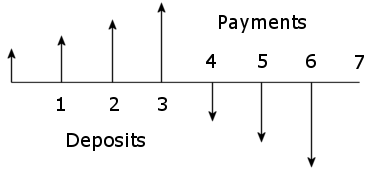

Copying a simple example from here, showing 4 deposits and 3 withdrawals.

Planning to retire in 4 months and draw monthly income of £1000 (present value) for 3 months, adjusted for inflation. APR is 8% and inflation is 4%. What should the pot be?

Calculating the monthly rates, assuming effective annual rates.

inf = 0.04;

i = (1 + inf)^(1/12) - 1 = 0.00327374

apr = 0.08;

m = (1 + apr)^(1/12) - 1 = 0.00643403

To illustrate the calculation, say we know at month 3 immediately after the final deposit, the pension pot p should be £3010.57

In month 4 it will have grown by (1 + m) and the inflation adjusted withdrawal will be w (1 + i)^4, where w = £1000. So the pension will decrease like so

p = 3010.57

p = p (1 + m) - w (1 + i)^4 = 2016.78

p = p (1 + m) - w (1 + i)^5 = 1013.28

p = p (1 + m) - w (1 + i)^6 = 0

This can be calculated in one go using a formula

o = 4 . . the month number

n = 3 . . the number of months

p = 3010.57

((1 + i)^o (-(1 + i)^n + (1 + m)^n) w)/(i - m) + (1 + m)^n p = 0

and more usefully, it can be expressed as a formula for p

p = ((1 + i)^o (1 + m)^-n ((1 + i)^n - (1 + m)^n) w)/(i - m) = 3010.57

So we need £3010.57 in month 3 for inflation adjusted withdrawals of £1000.

Starting with deposit d and increasing it to compensate for inflation

p = d

p = p (1 + m) + d (1 + i)^1 = 2.00971 d

p = p (1 + m) + d (1 + i)^2 = 3.0292 d

p = p (1 + m) + d (1 + i)^3 = 4.05854 d

This can also be calculated with a formula

q = 3 . . the final month number

p = (d ((1 + i)^(1 + q) - (1 + m)^(1 + q)))/(i - m) = 4.05854 d

We know p = 3010.57

∴ d = 3010.57/4.05854 = 741.79

The above can be expressed as a formula for d

d = ((i - m) p)/((1 + i)^(1 + q) - (1 + m)^(1 + q)) = 741.79

So the first deposit will be £741.79

The next month the deposit will be £741.79 (1 + i) = £744.21 etc.

The first withdrawal will be £1000 (1 + i)^4 = £1013.16 etc.

Putting the steps together

inf = 0.04;

i = (1 + inf)^(1/12) - 1 = 0.00327374

apr = 0.08;

m = (1 + apr)^(1/12) - 1 = 0.00643403

o = 4 . . the first withdrawal month number

n = 3 . . the number of withdrawal months

w = 1000 . the present value of the withdrawal amount

p = ((1 + i)^o (1 + m)^-n ((1 + i)^n - (1 + m)^n) w)/(i - m) = 3010.57

q = 3 . . the final deposit month number

d = ((i - m) p)/((1 + i)^(1 + q) - (1 + m)^(1 + q)) = 741.79

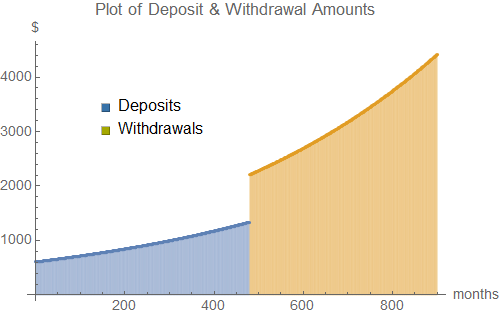

These same formulas can be used on a more realistically scaled calculation.

A more realistic calculation

For example, suppose someone at age 25 wants to withdraw $1000 per month present value from age 65 to 100. Inflation is 2% pa and interest is 3% pa (effective rates).

(65 - 12) * 12 = 480 deposit months

(100 - 25) * 12 = 900 months overall

inf = 0.02;

i = (1 + inf)^(1/12) - 1 = 0.00165158

apr = 0.03;

m = (1 + apr)^(1/12) - 1 = 0.00246627

o = 480

n = 420

w = 1000

p = ((1 + i)^o (1 + m)^-n ((1 + i)^n - (1 + m)^n) w)/(i - m) = 784011.41

q = 479

d = ((i - m) p)/((1 + i)^(1 + q) - (1 + m)^(1 + q)) = 606.00

They could achieve this by making 480 deposits, starting at $606 and increasing monthly in line with inflation: $607, $608, $609 etc.

The first withdrawal at age 65 will be $2208.04: $1000 present value, i.e. w (1 + i)^480.