Descriptions of the Kelly criterion are usually illustrated by examples about making optimal bets. But what would the guidelines be regarding using it to put together an optimal stock portfolio? For example the number of stocks to invest in, and the proportion to keep in cash?

1

-

2The key to using the Kelly criterion is having an accurate estimate of the odds on each possible bet. Coming up with those in the stock world is harder than the casino since there is a broad range of possible outcomes and evaluating likelihood of success is hard. Could someone have known early enough that Google would out do HotBot? Hard to estimate.– zeta-bandCommented Aug 6, 2018 at 20:25

Add a comment

|

2 Answers

The Kelly criterion was made famous by Edward Thorp, who invented card counting, implemented the Kelly criteria to manage his bets, later started a hedge fund, and subsequently became quite rich.

It just so happens that, being a mathematician by training, he wrote up a detailed paper, The Kelly Criterion in Blackjack, Sports Betting, and the Stock Market, on how to use the Kelly criterion. Fortunately, the paper is highly mathematical, and that acts as a gatekeeper to stop people who don't know what they're doing from just blindly taking a few equations and blowing themselves up.

But you asked, so I'll hand you the rope, which can be used to hang yourself. And you will hang yourself if you use these equations without understanding where they came from and what their limitations are.

If you have a portfolio of stocks which are uncorrelated with each other, the fraction of your bankroll that you should put in each stock is

f = (m - r)/s^2

where m is the expected return of the stock, r is the risk-free interest rate and s is the volatility of the stock.

If you have a portfolio of n stocks which are correlated, then this becomes

F = C^-1 (M - R)

where now F is the vector of fractions for each stock, C is the covariance matrix, M is the vector of expected stock returns, and R is the vector (r, r, r, ...).

Note how obviously risky this is. If you assume your stock has 11% expected returns, 15% volatility, and the risk-free rate is 6%, then this equations says you should put 222% of your portfolio in that stock. In other words, you should borrow money to invest in the stock market! And if you have more stocks in your portfolio, you should keep borrowing to add them! You will almost certainly go broke if you actually do this.

This is crazy. It's a result of our assumption that we really know what the expected return and volatility are, and, well, let me just quote Thorp:

Estimates of m in the stock market have many uncertainties and, in cases of forecast excess return, are more likely to be too high than too low. The tendency is to regress towards the mean. Securities prices follow a "non-stationary process" where m and s vary somewhat unpredictably over time. The economic situation can change for companies, industries, or the economy as a whole. Systems that worked may be partly or entirely based on data mining so [the true m] may be substantially less than [the expected m]. Changes in the “rules” such as commissions, tax laws, margin regulations, insider trading laws, etc., can also affect m. Systems that do work attract capital, which tends to push exceptional m down towards average values. The drift down means [the expected m] > [the true m] is likely.

Thorp actually advocates a "fractional Kelly" system, where you use some smaller fraction of the calculated allocation, and he has a discussion of this in his paper.

What it boils down to is this: A Kelly allocation is mathematical, and to use it properly, you have to construct your own model, using your own assumptions, keeping in mind your uncertainties and margin of safety. Similar to a civil engineer building a bridge, you can't just copy some formulas from your physics book and be sure your bridge won't crumble when a heavy truck drives over it.

If you want something less technical, I'd suggest that the Kelly criteria can be summarized as follows: You put more into the things you're more sure about and less into the things you're less sure about.

Using the Kelly Criterion for portfolio optimization isn't easy, which is why most discussions focus on simple bets with binary outcomes (i.e. win/lose). For stocks or other financial assets, you don't just win or lose and get a fixed payoff, instead you could win or lose and receive a vast, continuous range of returns like +10%, -5%, +3.267%. For a single stock and a risk-free asset, the formula becomes:

f* = (mu - r) / s^2

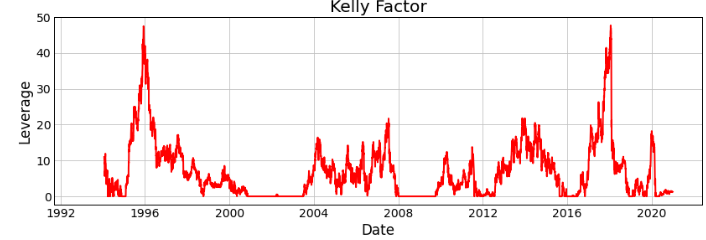

Where f* is the optimal fraction of your portfolio to invest in a position, mu is the expected return, r is the risk free rate, and s is the volatility. f* has no bound, so you can get these situations like this where the Kelly Criterion is claiming that it's optimal to place 50x leverage in the S&P 500:

This all depends on your estimates of volatility and excess returns of course, but even under reasonable assumptions you can get huge leverage results.

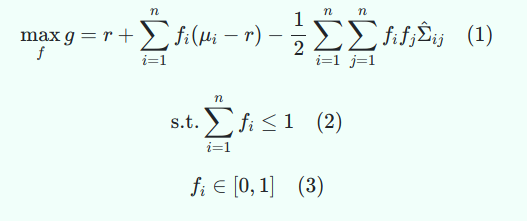

The formula for a portfolio is a bit more complex, this is actually an optimization problem. A common formulation of it is as a quadratic program which requires use of specialized algorithms to solve. We can write it like this:

This form optimizes it without leverage or shorts. Equation 2 says that you can only invest up to 100% of your portfolio in stocks or risky assets, which will keep you from taking on 50x leverage by following it blindly. You could modify this to put an arbitrary leverage cap on your portfolio in case you want to take on leverage (e.g. change the 1 to a 2).

You may be better off limiting each individual position though because if I understand the results in that post correctly, the model had a tendency to put all the money into a concentrated position (it's a narrow, optimization model after all) to get the biggest bang for its buck. So if you want to actually use something like this in practice, you could add a constraint where each f_i <= M, where f_i is the fraction you invest in an asset and M is the maximum position size for each asset. Then you'd need to define M so that if all assets were allocated to M, then your total portfolio's leverage would be equal to your maximum value. This would keep leverage to a reasonable level from a portfolio perspective, although you wouldn't be strictly Kelly-optimal in that case.