When a credit card transaction is in currency different to the one of the card, it is pretty normal for banks to charge a 1-3% fee associated with the currency conversion. Some banks do this by using their own conversion rates. Other banks charge a separate fee from the purchase while converting the purchase using rates from the payment system e.g. Visa/Mastercard. The latter is what all my cards' issuing banks do.

This question is about how those fees are handled on refunds. I have experience with credit cards from 4-5 banks in New Zealand, and all of them, except for one, handle it like this (excerpt from a real statement):

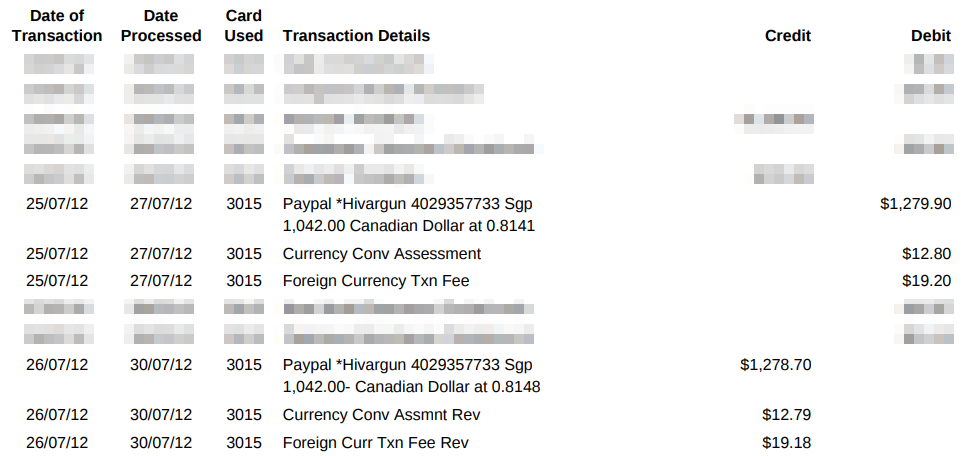

As you can see, the bank charged its fees in two separate lines ("Currency Conv Assessment" and "Foreign Currency Txn Fee"). What is important is that those fees were credited on the refund processed on 30 July 2012.

Now, one bank does this thing:

Essentially, it charges (debits) the fee on refund too — like it did on the original purchase. Whilst this is not contrary to their Credit Card Terms of Use (it is neither directly mentioned in there either, though), I am wondering:

- Which of the two practices is considered "normal", if any;

- Are there any costs that banks incur on processing foreign currency refunds (that are caused directly by those refunds being in foreign currency) that would justify debiting the fee on refunds as in the second example?