I've seen enough info out there comparing lump-sum investments into ETFs vs mutual funds with respect to broker commissions in the case of ETFs, and the discrepancy between MERs between the two. In that case, it's quite easy to figure out the threshold lump-sum to make a case for investing in an ETF instead of an equivalent mutual fund (typically a few $1000s).

What I'm trying to figure out now is given that I'm making monthly contributions to an index mutual fund with the MER of 1.00%, how would my overall expenses change if I switch to the equivalent ETF XIU with a MER 0.17%. My analysis compares a monthly contribution to the index fund with an equivalent purchase of ETF units. The analysis also includes broker commissions, which I'm taking to be $5/trade at Questrade.

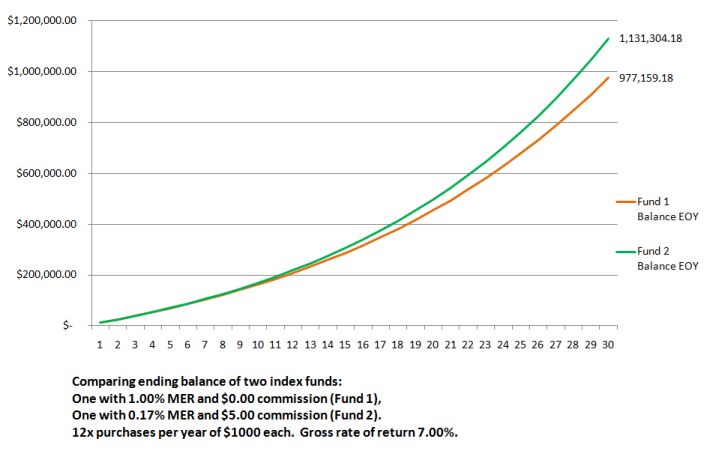

For example, say I contribute $1000/mo to my index fund. For ETFs, this purchase frequency would likely be too costly so I'd likely purchase new units every 6 months and contribute $6000 each time, or every 12 months for $12000.

I've started a spreadsheet, but no matter what my monthly contribution is, the mutual fund always seems to win. I'm likely calculating something wrong.

Ignoring the attached spreadsheet, is there either a quick and dirty ballpark method or a proper calculated method that I can use to determine (1) my purchase frequency and (2) the threshold investment amount?

Thanks in advance.

(I posted this question at the Financial Webring forum as well.)

EDIT

I was calculating a few things wrong so I updated the spreadsheet. Now the ETF wins.