With a few details missing from your question, I'm going to assume something. The reason why you're even considering this.

The minimum payment of the sum you'll borrow at the higher rate appear lower than the all the minimums you have now. It's similar to this -

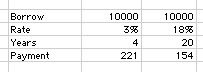

You see, if I borrow $10K at 3%, but have a 4 year payoff, my payment is $221. And a friend says "Joe, you're not so smart, my payment is only $154." The payment is lower, of course, but the term went from 4 years to a full 20.

With 6 cards I'd be curious what the balance is on each. If they are all $500, you make the minimum payments on each, except on the highest rate card, pay all you can. When that card is at 0%, you don't cut it up. You just regained the grace period, i.e. the charges made have no interest if you pay in full when you get the bill. Don't charge more than you can pay in full, use this card the way responsible users do, for the convenience, and safety, but no interest. At this point, you still pay the minimums on the lowest rate 4 cards remaining, and hack away at the next one, the highest remaining rate card.

With no background on your situation, I'd suggest you find a way to make a few hundred dollars per month. Our food bill is about $10/day/person, for example. We can only cut that back so far. But get a part time bit of weekend work, and you can probably make $200/weekend extra. That would pay off all this debt in 15 weeks just with this money.