What is Amortization?

An amortization schedule is often used to produce identical payments for the term (repayment period) of a loan, resulting in the principal being paid off and the debt retired at the end of the loan. This is in contrast to an interest only, or balloon loan. These loans require little or no payment against the balance of the loan, requiring the loan to be paid indefinitely if there is no term, or requiring the loan to be entirely paid off from cash or a new loan at the end of the term.

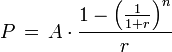

A basic amortization formula can be derived from the compound interest formula:

This formula comes from the Wikipedia article on amortization. The basics of the formula are the periodic payment amount, A (your monthly payment), can be determined by the principal loan, P, the rate, r, and the number of payments, n.

Why Amortize?

Lenders lend money to make a profit on the interest. They'd like to get back all the money they lent out. Amortization schedules are popular because the fixed low payments make it easier for borrowers to pay the loan off eventually. They also tend to be very profitable for lenders, especially at the start of the term, because they make a lot of profit on interest, just like the start of your mortgage.

The principal of a mortgage has more meaning than the principal of a revolving debt credit card. The mortgage principal is fixed at the start, and represents the value of the collateral property that is your home. You could consider the amount of principal paid to be the percentage of your home that you actually own (as part of your net worth calculation).

Credit Card Amortization

A credit card has a new balance each month depending on how much you charge and how much you pay off. Principal has less meaning in this case, because there is no collateral to compare against, and the balance will change monthly. In this case, the meaning of the amortization schedule on your credit card is how long it will take you to pay off the balance if you stop charging and pay at the proscribed payment level over the term described. Given the high interest rate on credit cards, you may end up paying twice as much for goods in the long run if you follow your lenders schedule.

Who Amortizes?

Amortizing loans are common for consumer loans, unless a borrower is seeking out the lowest possible monthly payment. Lenders recognize that people will eventually die, and want to be paid off before that happens. Balloon and interest only bonds and loans are more commonly issued by businesses and governments who are (hopefully) investing in capital improvements that will pay off in the long run. Thousands of people and businesses have gone bankrupt in this financial crisis because their interest only loans reached term, and no one was willing to lend them money anymore to replace their existing loan.