I'd like to ask about a different payment method to this question. I use THEAO's first-rate answer there.

How much profit or rate of return is required from a financial instrument, say stocks, to break even with a loan taken out for this? I'll use specific numbers to simplify –

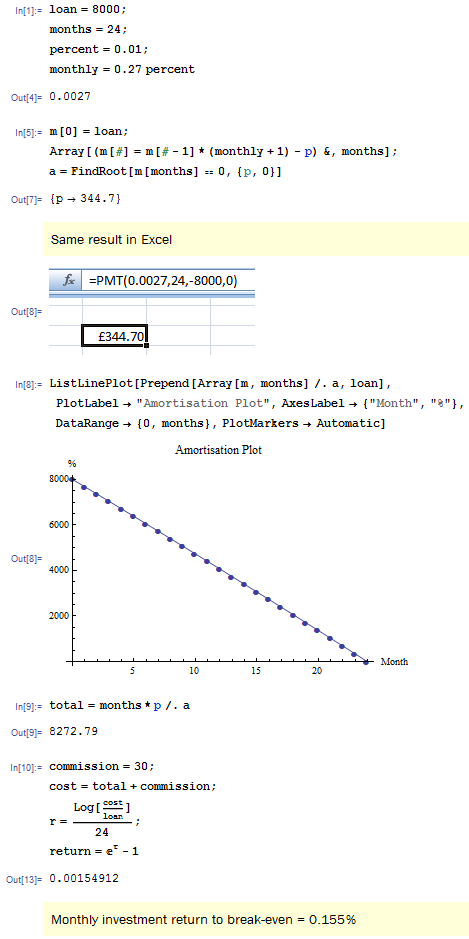

Suppose a bank gives – ☻ Loan = 8,000 USD, ☻ Months = 24, ☻ Monthly interest rate = 0.27%,

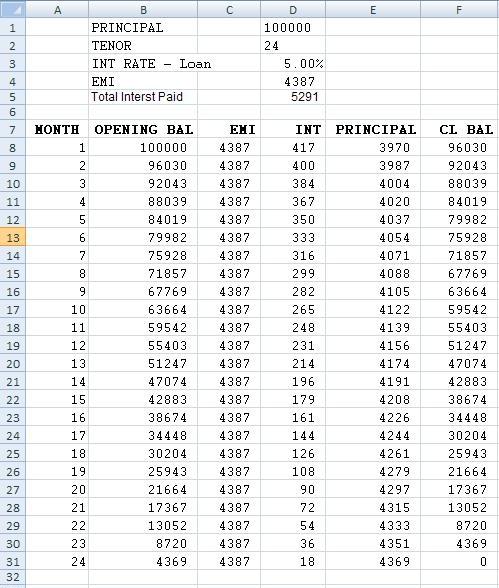

Then total amount of loan interest = 0.27%($8000)(24) = $518.4☻ The loan must be paid back in monthly installments so Excel's PMT(.027, 24, -8000, 0) = $344.70.

☻ Monthly income (say from job salary) = I. So I > $344.70.

☻ Tax rate = T. Of course, 0 ≤ T < 1. Then (1 – T)(Breakeven Amount) = Capital gain after tax.

I pay off the monthly installments only with my monthly employment income I. I'd hold onto the stocks bought in the first month for the 24 months. So only 1 commission for the sell – say $30.

Then (1 – T)(Breakeven Amount) = = 518.4 + 30 USD. I'll round up to 550.

So Breakeven Amount (Call this B) = 550/(1 – T).

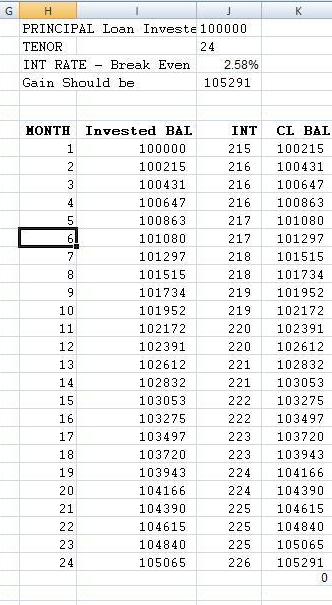

So I'll breakeven on this loan -– if and only if – I make 550/(1 – T) over 24 months (so the rate of return is B / (10000 + B)).

Anything wrong here? This feels too simple? Are there better ways to think about all this?

Also, what's the best strategy with using a loan to invest in a financial investment?

EDIT after THEAO's answer – I'll assume the monthly income is from employment.

Let me know if this thinking is wrong. I'm just focused on breaking even/recouping – at least – with the total cost of this loan. Is it right that the total cost of this loan is just the total amount of loan interest from stocks over 24 months ($518.4) ? I thought the loan principal ($10,000 USD) is repaid. So it's not part of the cost of this loan. So I'm not expecting stocks to make me/gain the loan principal.

So in your answer, I'm not expecting an income of $344.70 from the stocks every month. I'd only expect one investment income – at the end of the 24 months – the (hoped for) profit which is at least the total cost of the loan.

Does this change anything?

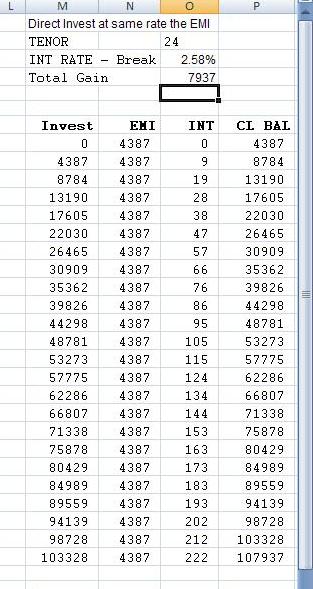

I also thought about using my monthly salary to keep buying shares every month. But then, if the stock price goes up over the 24 months, there'd be less profit. As the price goes up, I'd buy fewer months every month. But with the loan, I can buy many more shares in the 1st month. Don't I just need to breakeven on the total cost of the loan over the 24 months?