I’m trying to arrive at a formula that allows me to determine the future value of a present savings amount (P), given the following:

Period (p): e.g., Annual (p=1), Semiannual (p=2), Quarterly (p=4), Monthly (p=12) Years of withdrawals: y Annual withdrawal amount: W Annual savings growth percent: r Periodic savings growth rate: m = (1+r)^(1/p)-1 Annual inflation percent: i

I found a formula on this forum that allows for the above, based on withdrawals at the END of the chosen period as follows:

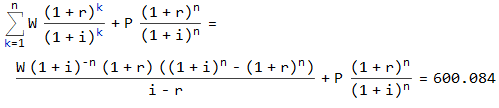

FV = W/p*(r/m)[(1+i)^y-(1+m)^(yp)]/(r-i) + P*(1+m)^(y*p)

I was able to modify it to allow withdrawals at the beginning of the chosen period as follows:

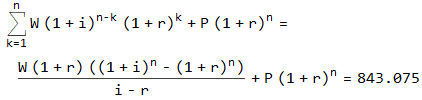

FV = W/p*(1+1/m)[(1+i)^y-(1+m)^(yp)]/(r-i) + P*(1+m)^(y*p)

But the above formulas provide errors when i = r. I’ve been trying to arrive at a general formula that allows the inflation rate to equal the savings rate.

Can anyone help?

Thanks in advance.