Let's ignore the transaction fees from my broker, which tend to be higher for the secondary market. Are there any other downsides of purchasing bonds on the secondary market instead of the primary market? If that depends on the location, my main interest is the US.

asked Feb 26, 2023 at 23:28

-

1If you purchase them at a discount, you’ll eventually have to pay capital gains tax. Also, typically you’ve got to buy a lot of bonds on the primary market.– RonJohnCommented Feb 27, 2023 at 5:38

-

@RonJohn Thanks! "you’ll eventually have to pay capital gains tax. " even if hold until maturity? "typically you’ve got to buy a lot of bonds on the primary market" Do bonds typically have lower minimum purchases on the secondary market than on the primary market?– Franck DernoncourtCommented Feb 27, 2023 at 5:41

-

1On capital gains: I’m pretty sure. If you buy it for $950 and it’s redeemed for $1000, you have $50 in capital gains.– RonJohnCommented Feb 27, 2023 at 5:44

-

1On the quantity: look at your broker’s fixed income web page to see how many bonds are for sale. It’ll show you the minimum purchase for each.– RonJohnCommented Feb 27, 2023 at 5:47

-

@RonJohn I posted more details about the tax on muni discounts. Thanks very much for pointing to it!– Franck DernoncourtCommented Mar 10, 2023 at 4:06

Add a comment

|

1 Answer

One downside of purchasing municipal bonds (aka munis) on the secondary market instead of the primary market, as RonJohn mentioned in the comment section: municipal bonds on the secondary market may be discounted, and this discount is taxed.

Schwab has two good articles authored by Cooper Howard on it:

Key takeaways from these two articles:

Municipal bonds, or munis, are usually issued with a $1,000 par value, which is the amount you can expect to receive when the bond matures. However, after the initial issuance date, a muni’s value can rise and fall in the secondary market. Events such as rising interest rates or deteriorating credit quality can cause the value of the bond to fall below $1,000. When that happens, the bond is trading at a discount.

Tax treatment of muni discount:

Let's say you want to buy a $10,000 muni currently trading at $9,750—a $250 discount. When the bond matures in five years, barring default, you would receive the full par value of $10,000, meaning you would earn $250 on the bond plus the coupon income. What many investors may not realize is that they could owe taxes on that $250 discount.

Discounts are taxed using the de minimis rule, which uses the size of the discount to determine whether it will be taxed as capital gains1 or ordinary income:

A discount of less than 0.25% for each full year from the time of purchase to maturity is taxed as a capital gain.

A discount of 0.25% or more for each full year from the time of purchase to maturity is taxed as ordinary income.

Returning to our example, you'd multiply the par value by the percentage threshold of 0.25% and the number of full years to maturity ($10,000 x 0.25% x 5), which gives you a dollar threshold of $125.

Consider an original-issue-discount muni: Occasionally, a municipality will issue bonds at a discounted price, known as an original issue discount (OID). For such bonds, the OID is treated as part of the bonds' interest income and is usually exempt from capital gains and ordinary income taxes. (An OID bond trading in the secondary market, on the other hand, is subject to all the rules of a regular bond.)

The purchase date matters: If you acquired a discount muni before April 1993, you’ll have to pay capital gains tax only.

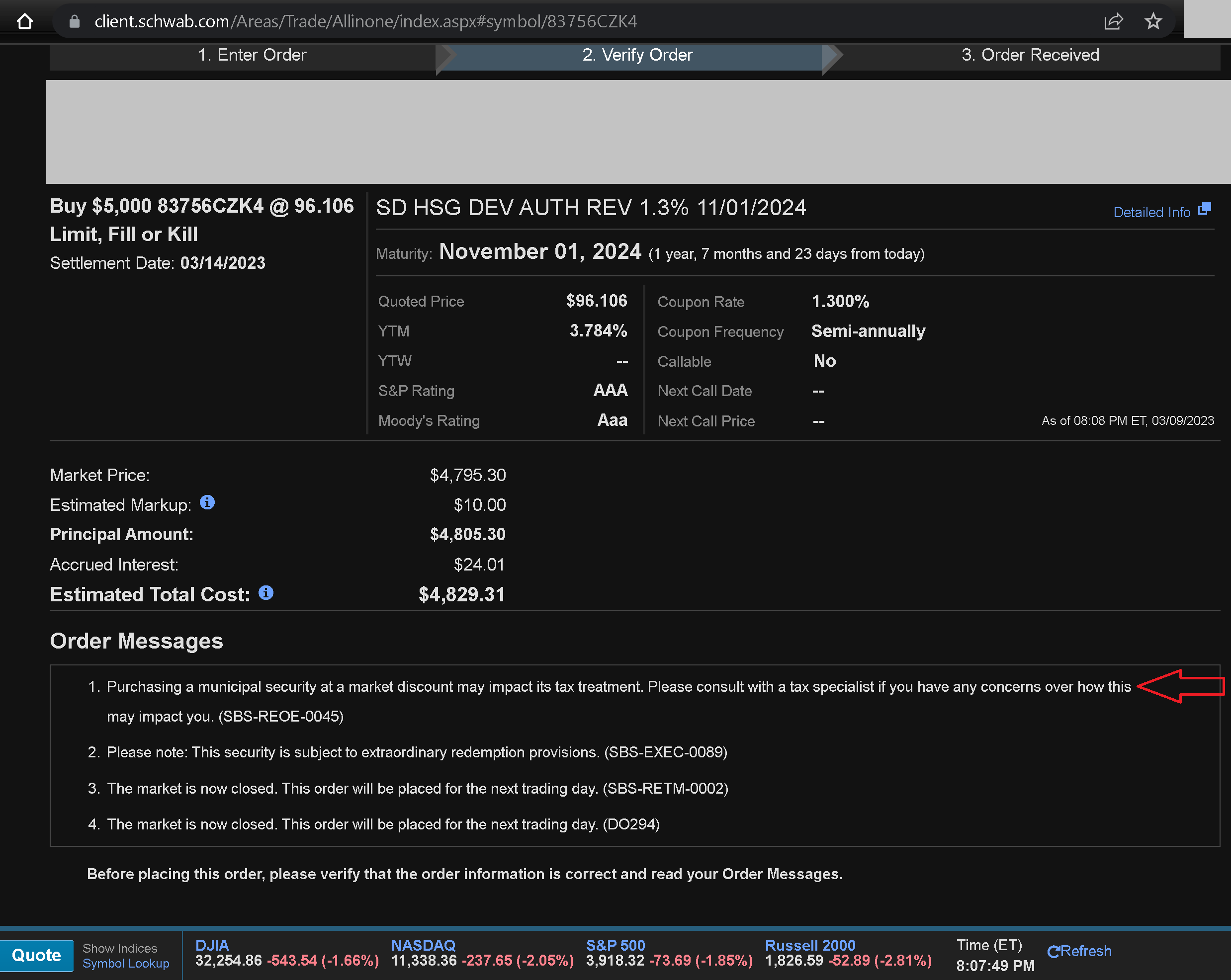

Some brokers warn their clients about muni discount taxes, e.g. Schwab:

answered Mar 10, 2023 at 4:05