If you buy Zero Coupon Bond (Tax Exempt), can it go down in price?

For example: This bond is costing 18 USD now and it will give back 100 at maturity, can it cost 17 tomorrow?

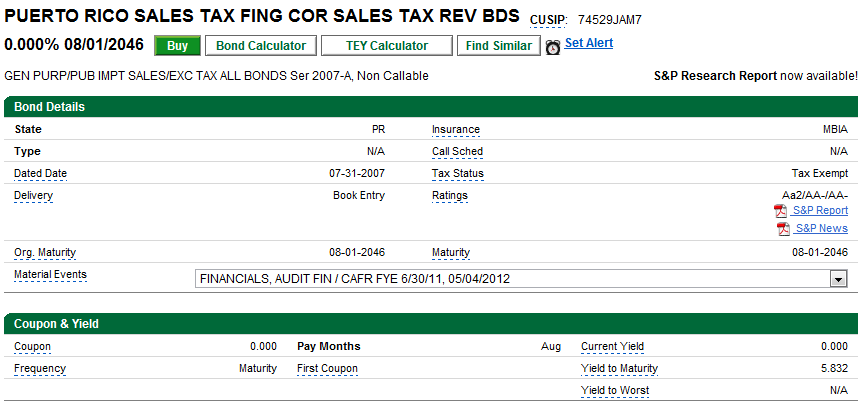

If you buy Zero Coupon Bond (Tax Exempt), can it go down in price?

For example: This bond is costing 18 USD now and it will give back 100 at maturity, can it cost 17 tomorrow?

Of course it can. This is a time value of money calculation. If I knew the maturity date, or current yield to maturity I'd be able to calculate the other number and advise how much rates need to rise to cause the value to drop from 18 to 17.

For a 10 year bond, a rise today of .1% will cause the bond to drop about 1% in value. This is a back of napkin calculation, finance calculators offer precision.

edit - when I calculate present value with 34 years to go, and 5.832% yield to maturity, I get $14.55. At 5.932, the value drops to $14.09, a drop of 3.1%.

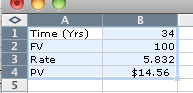

Edit - Geo asked me to show calculations. Here it goes -

A) The simplest way to calculate present value for a zero coupon bond is to take the rate 5.832%, convert it to 1.05832 and divide into the face value, $100. I offer this as the "four function calculator" approach, so one enters $100 divided by 1.05832 and repeat for the number of years left. A bit of precision is lost if there's a fractional year involved, but it's close. The bid/ask will be wider than this error introduced.

B) Next - If you've never read my open declaration of love for my Texas Instruments BA-35 calculator, here it is, again. One enters N=34 (for the years) FV = 100, Rate = 5.832, and then CPT PV. It will give the result, $14.56.

C) Here is how to do it in Excel -

The numbers in lines 1-3 are self evident, the equation in cell B4 is =-PV(B3/100,B1,0,B2) - please note there are tiny differences in the way to calculate in excel vs a calculator. Excel wants the rate to be .05832, so I divided by 100 in the equation cell.

That's the best 3 ways I know to calculate present value. Geo, if you've not noticed, the time value of money is near and dear to me. It comes into play for bonds, mortgages, and many aspect of investing. The equations get more complex if there are payments each year, but both the BA-35 and excel are up to it.

Certainly, yes, a zero coupon bond can go down in price.

If interest rates rise before your bond matures, the price of the bond will go down – and the longer to maturity, the more it will tend to drop. Depending on when you bought and how much interest rates rise, you can incur a capital loss.

The bond is guaranteed to be worth a certain amount at maturity as long as the issuer hasn't defaulted, but before maturity the market price of the bond will fluctuate, primarily based on interest rate movements. In fact, zero coupon bonds are even more interest-rate-sensitive than regular bonds (which have periodic coupon interest payments.)

Let's say today you buy the bond issued by StateX at 18$.

Let's say tommorow morning the TV says that StateX is going towards default (if it happens it won't give you back not even the 18$ you invested).

You (and others that bought the same bond like you) will get scared and try to sell the bond, but a potential buyer won't buy it for 18$ anymore they will risk maximum couple of bucks, therefor the price of your bond tomorrow is worth 2$ and not 18 anymore.

Bond prices (even zero coupon ones) do fluctuate like shares, but with less turbolence (i.e. on the same period of time, ups and downs are smaller in percentage compared to shares)

EDIT: Geo asked in the comment below what happens to the bond the FED rises the interest. It' very similar to what I explained above.

Let's say today you buy the bond just issued by US treasury at 50$. Today the FED rewards money at 2%, and the bond you bought promised you a reward of 2% per year for 10 years (even if it's zero coupon, it will give you almost the same reward of one with coupons, the only difference is that it will give you all the money back at once, that is when the bond expires).

Let's say tommorow morning the TV says that FED decided to rise the interest rates, and now on it lends money rewarding a wonderful 4% to investors. US treasury will also have to issue bonds at 4%.

You can obviously keep your bond until expiration (and unless US goes default you will get back all your money until the last cent), but if you decide to sell your bond, you will find out that people won't be willing to pay 50$ anymore because on the market they can now buy the same type of bond (for the same period of time, 10 years) that give them 4% per year and not a poor 2% like yours. So people will be willing to pay maximum 40$ for your bond or less.