Final Edit: End Value of 60/40(10-Year Treasury) is worse than S&P 500.

Instead of blindly deriving the Bonds Fund price from Yield to Maturity, this time using the oldest available proxy to 10-Year Treasury Index (i.e. Lehman/Barclays/Bloomberg) which are the following Mutual Funds in 6:4 Ratio:

- Vanguard Intermediate-Term Treasury Fund Investor Shares (VFITX), duration 5.2 years, inception 10/28/1991

- Vanguard Long-Term Treasury Fund Investor Shares (VUSTX), duration 18.0 years, inception 05/19/1986

and:

- Vanguard Total Stock Market Index Fund Investor Shares (VTSMX), inception 04/27/1992

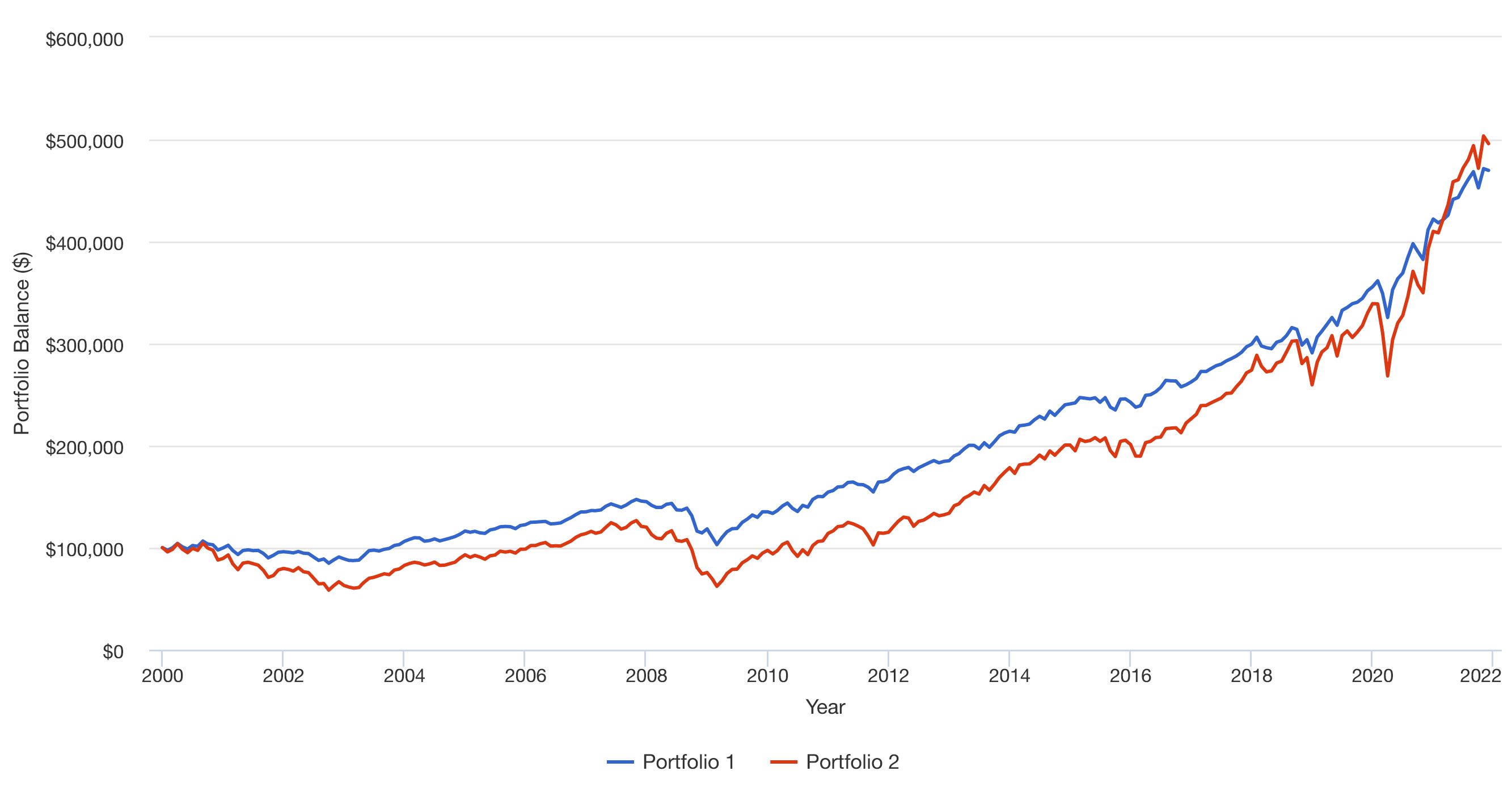

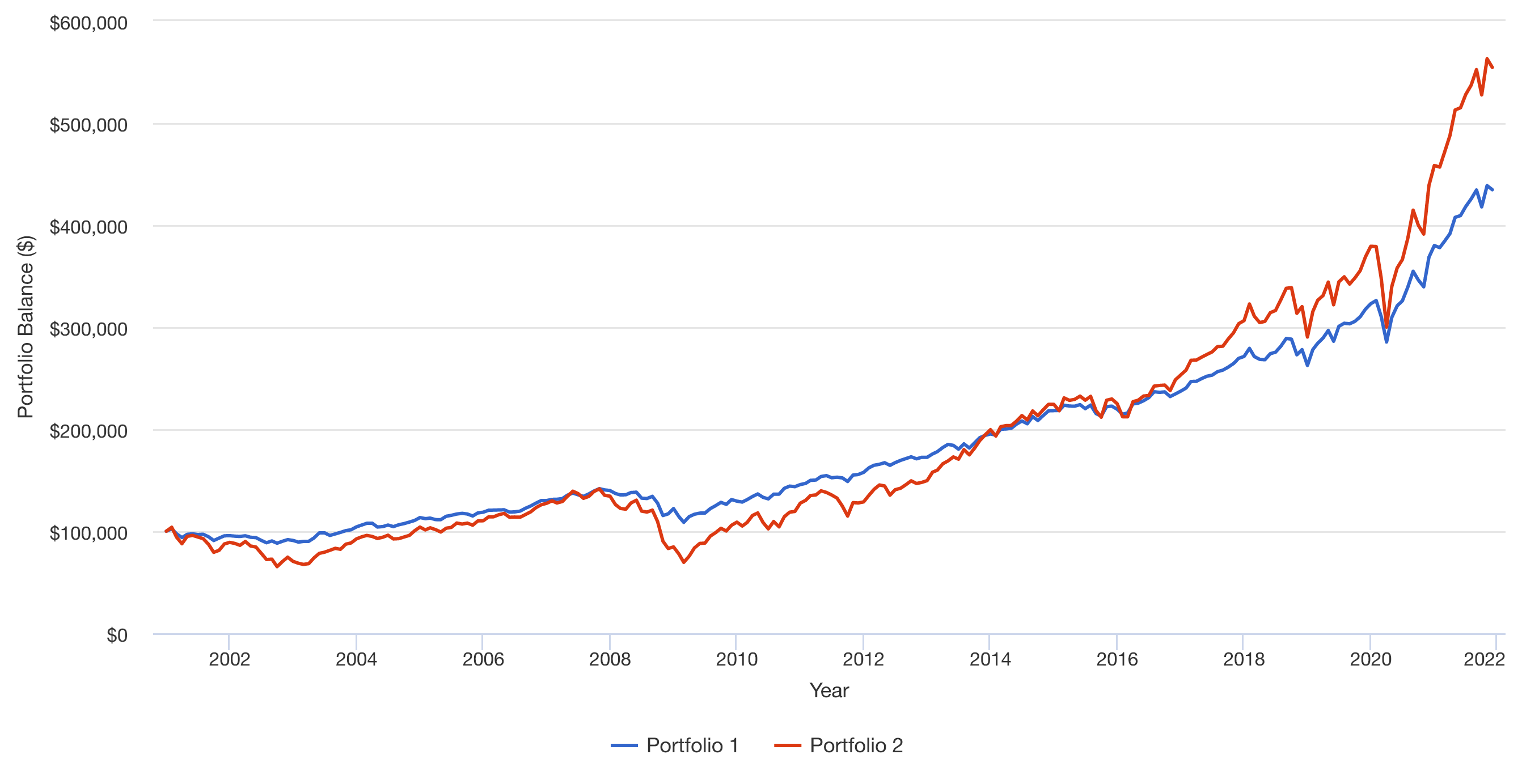

In the following charts:

- Portfolio 1 represents 60% S&P 500 (VTSMX), 24% VFITX + 16% VUSTX (10-year Treasury)

- Portfolio 2 100% S&P 500 (VTSMX)

Assume Montly Rebalancing because that is how balanced funds and the index works.

$100k Lump Sum with Monthly Rebalancing = False

$100k Lump Sum and $5k Monthly Dollar Cost Averaging with Monthly Rebalancing = False

Edit: After discussing with the author on their assumptions.

I hope we can settle the claim once and for all.

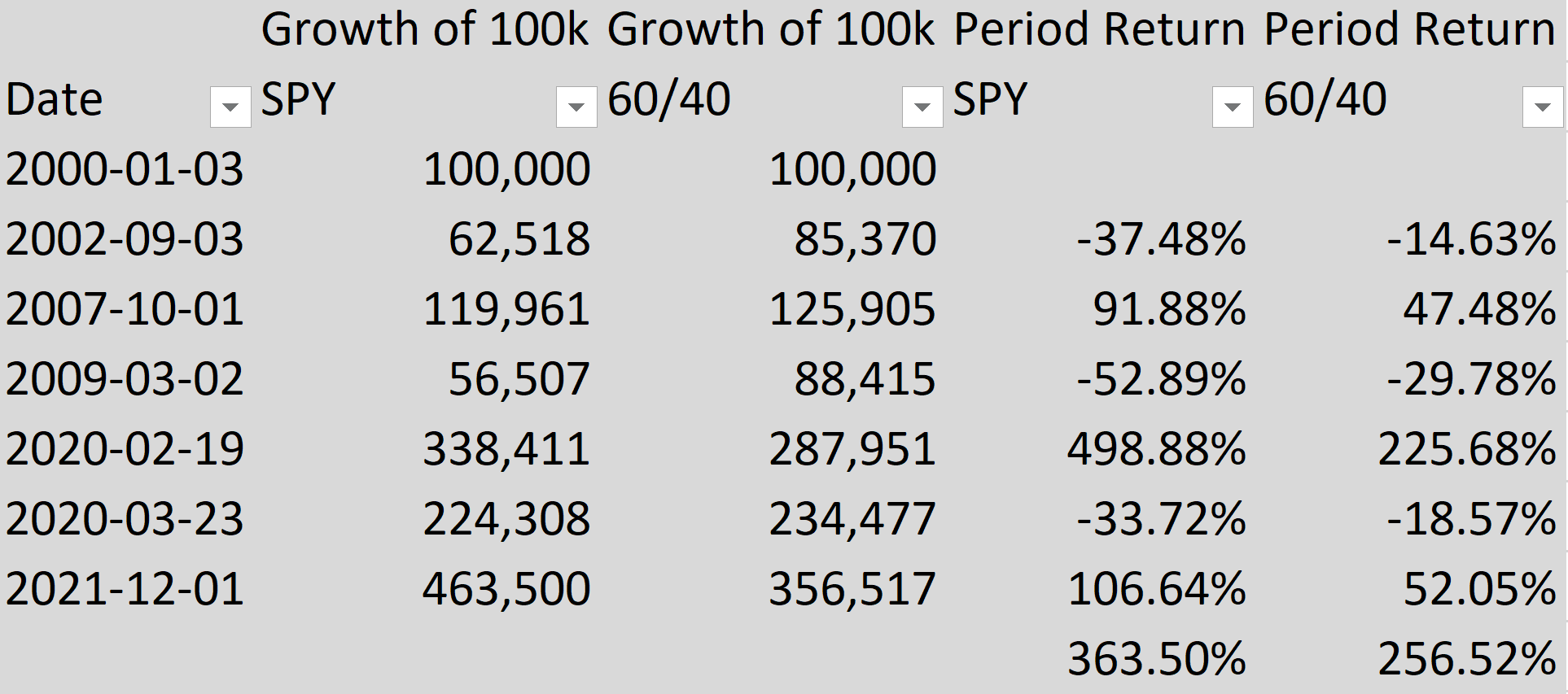

- S&P 500 = Adjusted Close with Yahoo Finance

- 10-year Treasury = Yield to Maturity from macrotrends.net, which I confirmed it to be extremely similar to treasury.gov

- Start Date = 2000-01-03

- End Date = 2021-12-01

- Lump Sum $100,000 with no additional funds

- Reinvested dividend

- "Continous Rebalancing" = Assume Daily Rebalancing

- No Bid/Ask Spread (theoretically TLH has 0.05% spread, which does add up daily.

- No Capital Gains or Divividend Tax

- Price of Bonds Fund = 100/((1+YTM/100)^10)

- A very smart Bonds Fund manager is able to maintain constant maturity (theoretically a 10-year Bonds becomes 9.997-year Bonds after 1 day. )

Result: End-Value of 60/40 is worse than 100% S&P 500.

Raw Data, Formula, and Excel files here:

https://www.mediafire.com/file/p34fe2y7td4dchx/6040_vs_SPY.xlsx/file

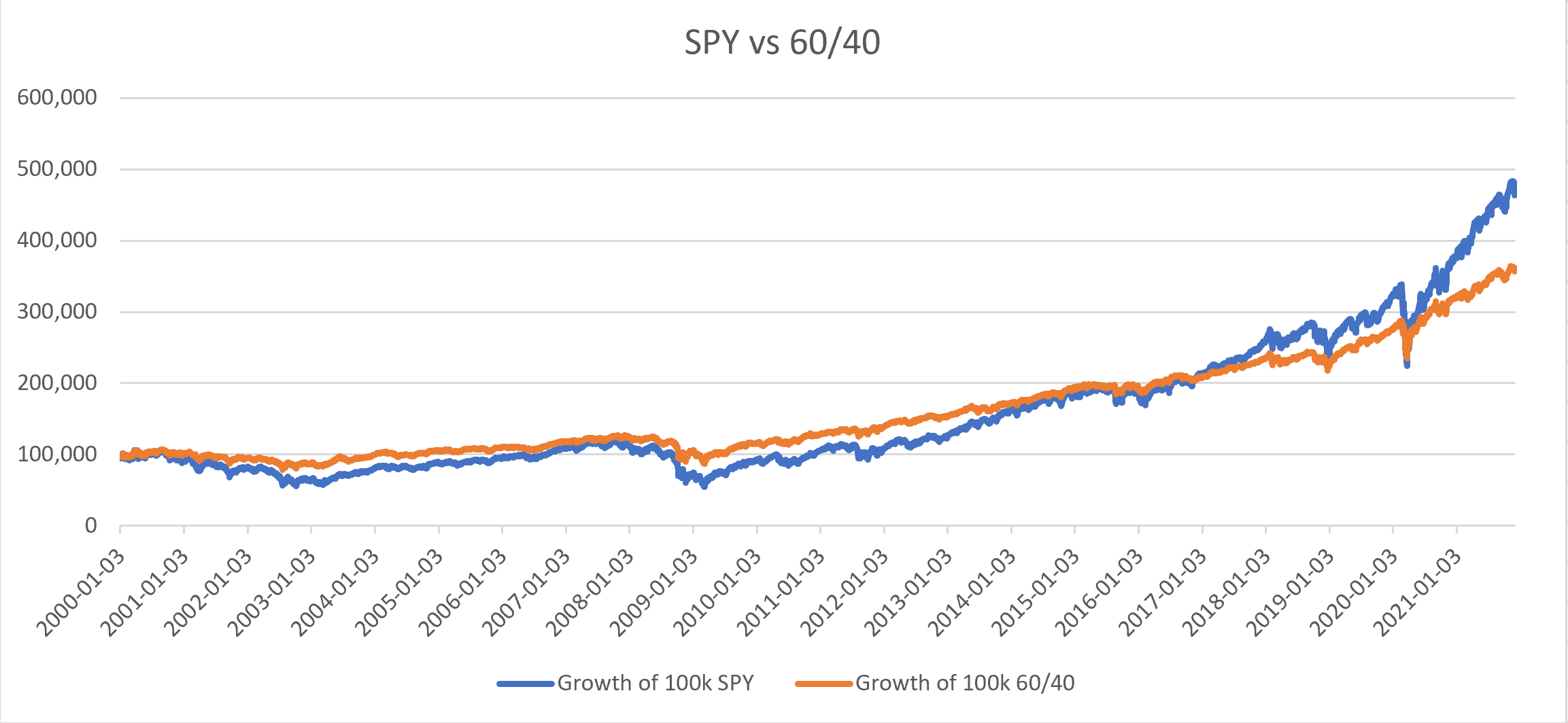

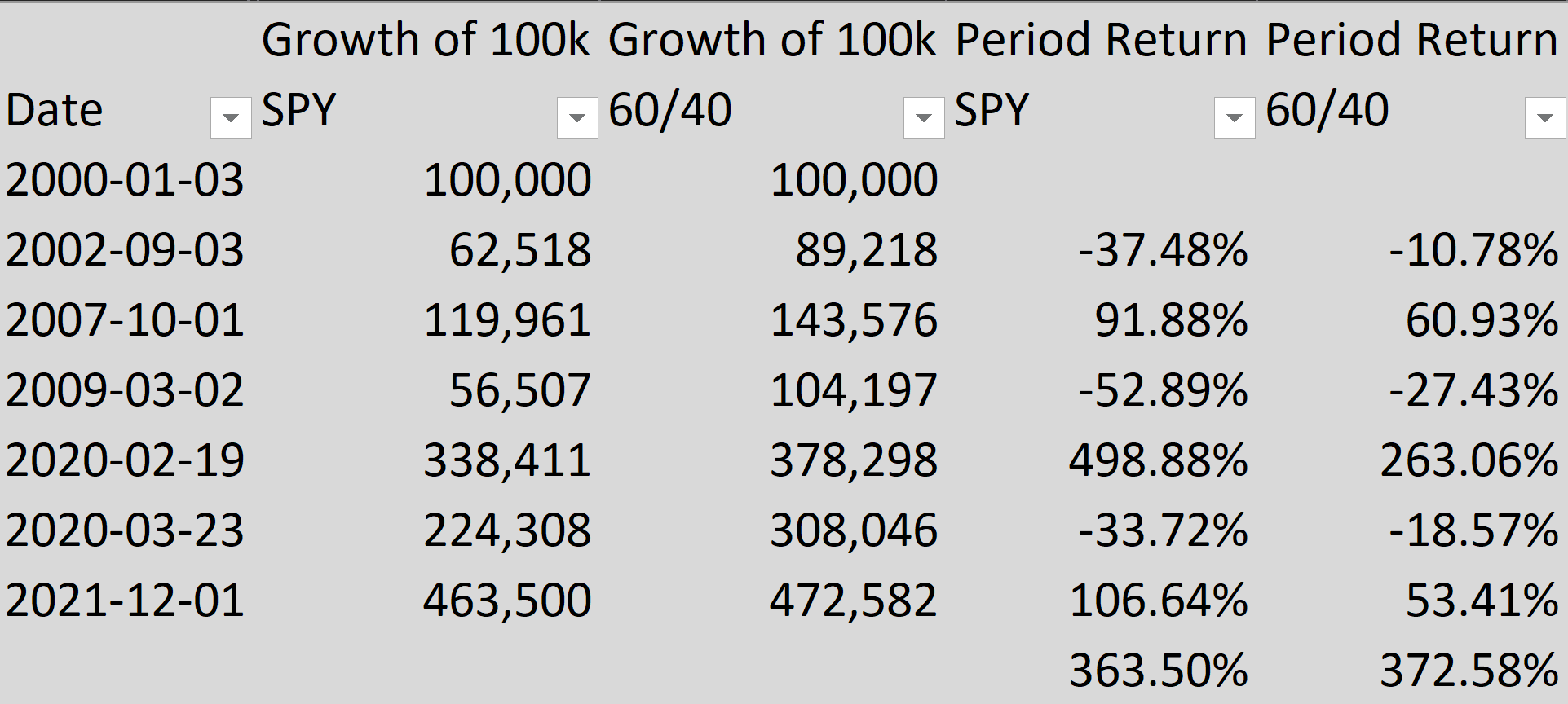

Edit 2: Using this calculation methodology (especially daily rebalancing) and including YTM that are realized (i.e. daily interest as income), the result is that 60/40 is slightly better than S&P 500.

However, practically this is debatable, especially when S&P 500 Total Return Index is much higher than Yahoo Finance Adjusted Return (372% vs 363%), and that Bonds market is inefficient with high bid/ask spread.

When using Passive Bonds Funds (Mutual Fund or ETF), I have yet to see that this calculation methodology is realistic. If you go to Morningstar and look for Active Balanced Funds since 2000, there will always be Outperforming Funds and Underperforming Funds. But if you look at those benchmarked at S&P 500/AGG, the outperformance with 100% S&P 500 didn't happen.

For example, using this calculation methodology, the total return from 2008 to 2021 is 225%, yet when using 60% SPY, 28% IEF, 12% TLH, it is 219%.

This further reinforces that deriving Bonds Price with only Yield to Maturity is an incorrect method, and that this discussion should have started with Total Bonds Market Index with monthly rebalancing, minus realistic tracking error, to begin with.

Still, it is not known how the author calculated 425.9% total return for 60/40 Portfolio.

Raw Data, Formula, and Excel files here:

https://www.mediafire.com/file/n7unzo2kypjhk5n/6040_vs_SPY_with_Bonds_Interest.xlsx/file

If you look at the definition of "60/40 stock/bond portfolio" at 24:14 of the video, it says:

60/40 is 60% S&P 500 and 40% 10-year Treasury

This is the part where it is misleading. Treasury Bonds had a magnified great run in the past 20 years. The longer the duration of the Treasury, the higher return and lower volatility it brings.

This 60/40 is different from the Modern Portfolio Theory, where the "Market Portfolio" is 60% Total Stock Market and 40% Total Bonds Market (including Treasury, Corporate, Municipal, Junk, etc).

So instead of 40% BND ETF that Bogleheads recommended, the 10-year Treasury is simulated by IEF ETF and TLH ETF on a 7:3 Ratio.

They could have made it more misleading by using 20-25 years Treasury (i.e. TLT and EDV ETF).

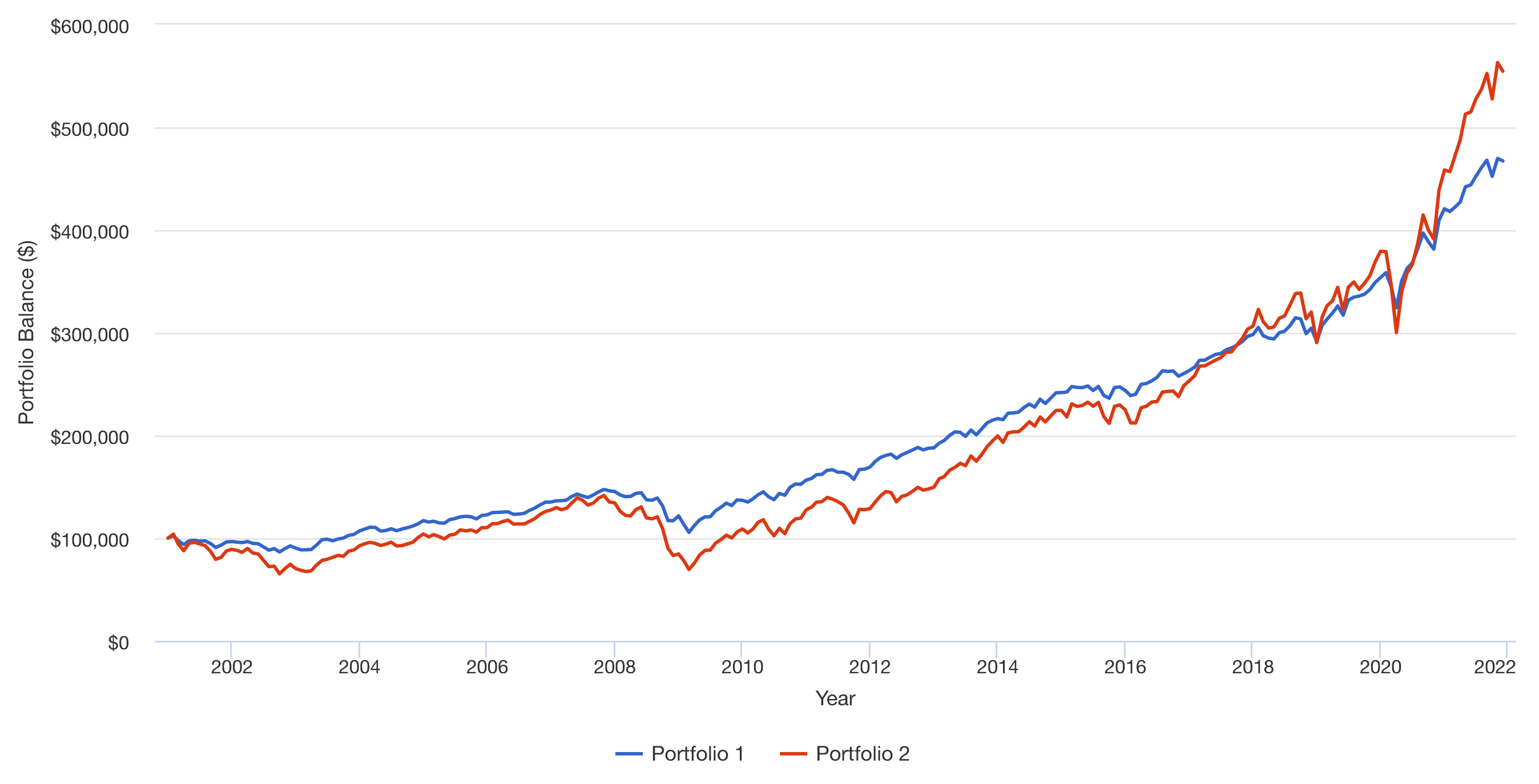

Back to your question #1 and #2. In the following charts:

- Portfolio 1 represents 60% S&P 500 and 40% 10-year Treasury

- Portfolio 2 100% S&P 500

Asseume Reinvested Dividend/Interest.

$100k Lump Sum with No Rebalancing = False

$100k Lump Sum with Quarterly Rebalancing = False

I would not spend a minute of my life watching such videos.

{kind=link}