House-hacking is probably the most effective thing you can do for your financial runway. Craig Curlop covers this strategy intensively in his book, The House Hacking Strategy. Its power is also fairly demonstrated in Scott Trench's book, Set For Life, which also covers the topic of investing and constructing one's financial plan for the everyday worker.

House-hacking is the act of purchasing a house and either renting out individual rooms or buying a multi-plex, such as a duplex, triplex, fourplex, etc, and renting out other sides while living in one. When bought right, this enables you to cut your housing expenses significantly, and in many cases live for free. It effectively turns your primary residence into an active investment that has the potential to generate cash-flow, or at the very least make your housing much cheaper than before (make sure to account for reserves; maintenance, CapEx, taxes, etc).

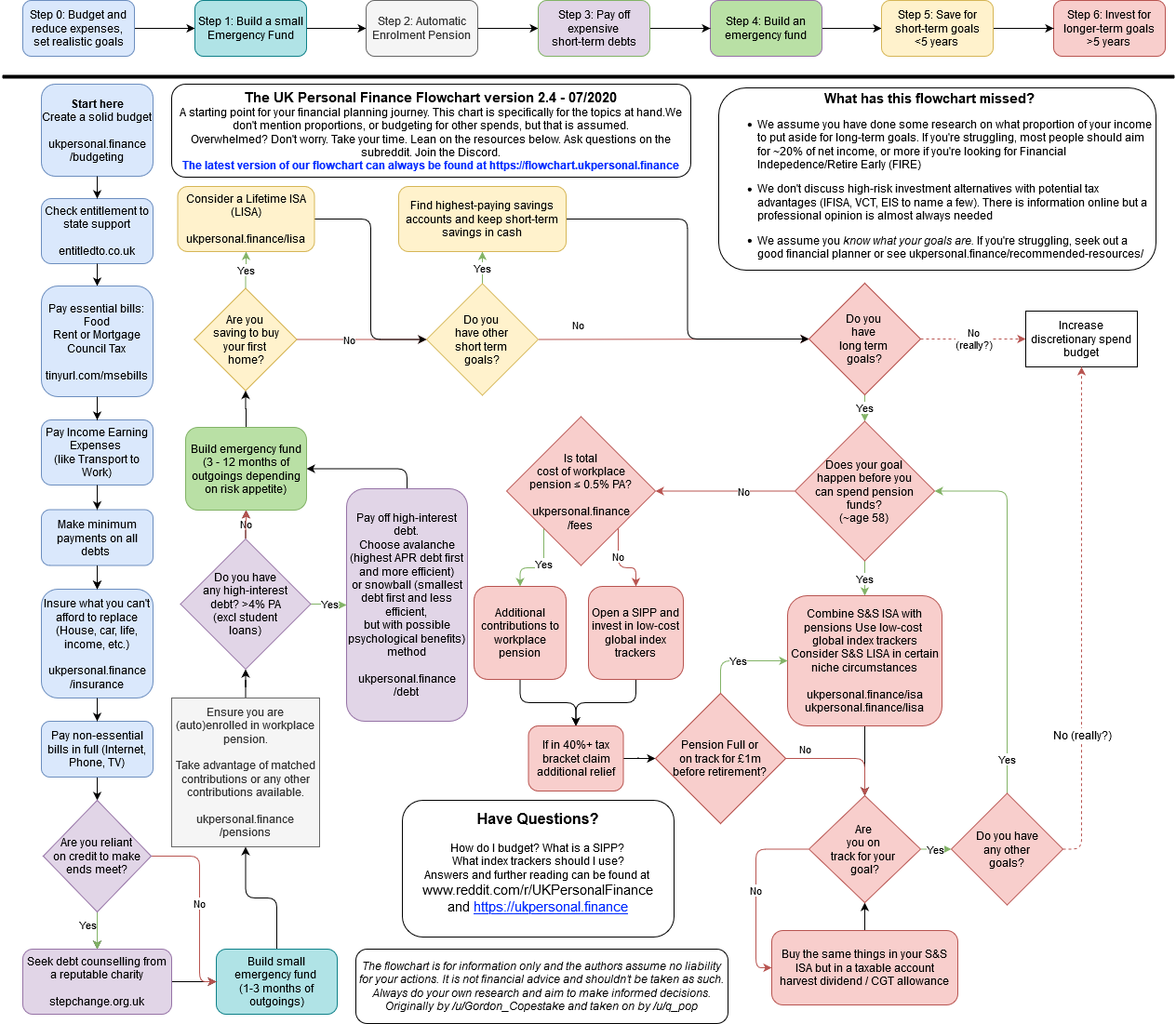

While taking advantage of employee retirement matches can be a viable option, I'm going to leave that discussion to someone more knowledgable in your country as the amounts, taxes, and penalties vary. Generally speaking, contributing to match the employer's match does make sense.

After implementing your first house-hack, you should choose between investing your remaining and future money in one of the following ways that make sense for your financial goals:

- in bonds (least volatile, but generally speaking the lowest gains in the long run), this usually makes sense for conservative people who are about to retire.

- low-cost index funds (higher volatility, better returns while paying minimum fees and just following the market's average returns), this usually makes senes for people who want maximum returns for the lowest amount of work, while having time to through the stock market's volatility. JL Collins has an excellent book on index-fund investing, The Simple Path to Wealth.

- further real estate investing (excellent returns, when you buy right, but requires more hands-on knowledge and proper education and understanding -- educate yourself). This makes sense for people who are willing to put in a lot of extra hours for excellent long term gains, based on a business model that's stood the test of time, assuming its based on proper execution. I'd recommend the forums, podcasts, and books published by Bigger Pockets if you want to learn more.

- at last consider investing in your own startup that focuses on a need that impacts scale or magnitude (most work, best potential returns -- with the chance of receiving nothing). This makes sense if you've already cut down most of your living expenses by house-hacking, and-or you're willing to spend 1-5 years of your life on something that may give you $0 or infinite returns. I personally like to refer people to MJ Demarco's books when covering this topic, primarily The Millionaire Fastlane, but if you're interested do your own research.

The most important factor when making your decision, which can result in your allocating your investing to one, some, or all of the asset classes mentioned, is to understand what you're investing in. While there are other options out there, I don't recommend them or I'm not knowledgeable enough to comment on them. Feel free to explore outside of this realm, but be truly educated, and no, a couple of gurus do not count as education.

Some will argue that buying physical assets that do not generate cash-flow or gain predictable appreciation, such as gold or silver, to be viable hedges against inflation and money being printed but I'll leave that for you to decide.

Whatever you do, don't throw your money into mutual funds that charge you 0.5-2% fees, while rarely even beating the market over the course of 20 years. Also, avoid speculating in individual stocks as its a losing strategy for 99.9% of us. The same goes for Crypto, it's not investing, it's speculating. Speculating and gambling is fine if you're aware of it and you're okay with the money being lost. Just don't call it investing.

Finally, focus on your goals. Bonds and index funds will not make you rich, they just maintain your money's worth, sometimes with a little bit of extra juice. Real estate and entrepreneurship can make you rich. Each asset class is a tool, it's up to you to decide which tools make sense for your goals. You may want to consult with a fixed-fee financial advisor (don't pay them % of your investments..) if you're not sure after reading this, and always consult with a CPA.