I keep hearing about the 4% rule. I know it's based on historic returns, but aren't those returns based on U.S. stocks, at a time when the U.S. was ascending to the peak of "world superpower" status? Has there been any studies on how the 4% rule would fare if the U.S. stock market returns to the mean of the rest of the industrialized world? Would it make any difference?

-

3According to you, when was the US at the peak of "world superpower" status? Because I remember this rule from the 1980s, and I'm pretty sure it's older than that.– RonJohnCommented Oct 8, 2019 at 16:55

-

1I'd say right around WWI all the up to recent times. It's roughly when the U.S. rose to dominance. Th original study was created using data from 1926 to 1976, but I believe people have studied it using more recent market returns. What I wanted to know is how does the 4% rule fare if you looked at worldwide stock market, rather than just the U.S.– NL3294Commented Oct 8, 2019 at 17:48

-

3For those of us who haven't been hearing about it, what is ‘the 4% rule’?– giddsCommented Oct 10, 2019 at 8:58

-

1@gidds it means Bengen, William P. (October 1994). "Determining Withdrawal Rates Using Historical Data". Journal of Financial Planning 171-180: in summary "...using the charts for a 50/50 stock/bond allocation, determine the highest withdrawal rate that satisfies the desired minimum portfolio life. For a client of age 60-65, this will usually be about 4 percent." retailinvestor.org/pdf/Bengen1.pdf– DavePhDCommented Oct 10, 2019 at 13:28

-

5@DavePhD Thanks. Wouldn't that be better in the question where everyone can see it?– giddsCommented Oct 10, 2019 at 13:30

|

Show 3 more comments

3 Answers

Not safe at all. A 4% withdrawal rate would require the US stock market in the 21st century to produce returns similar to those of the 20th century, i.e. in the vicinity of 7% in real (inflation-adjusted) terms. Fair estimates for stock returns going forward are not this high. Rick Ferri proposed a real 5% over a 30-year horizon in 2015. I recall Bernstein in his book "Rational Expectations" (2014) proposing a real 3.6% over the very long term. These long-term estimates are based on the Gordon equation. According to this model, the long-term growth of a 100% SP500 stock investment in real terms would be the current dividend yield (~2%) plus the expected per share dividend growth rate (often given as 2%).

Bernstein's opinion on this subject is as follows: "Two percent is bullet-proof, 3% is probably safe, 4% is pushing it and, at 5%, you're eating Alpo in your old age [...] If you take out 5% and you live into your 90s, there's a 50% chance you will run out of money." (Source)

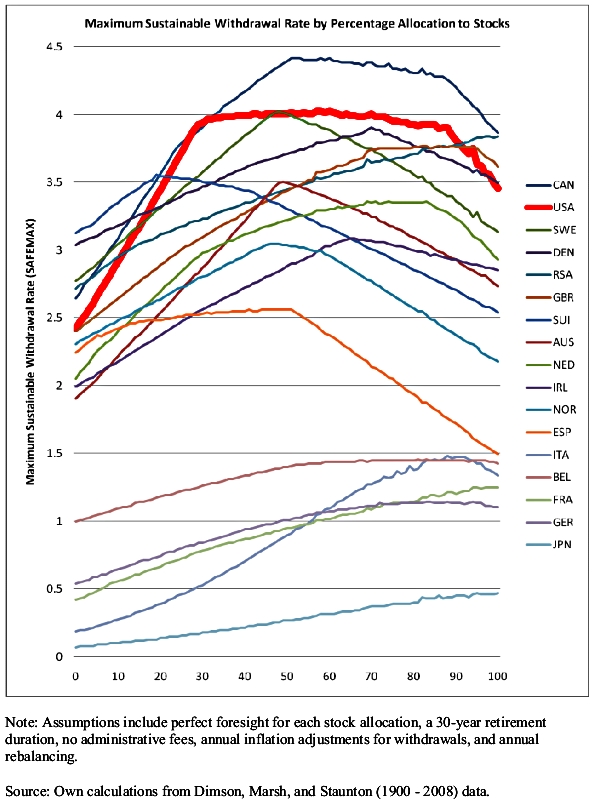

It is interesting to look at what happened to other countries in the past to get an idea of what could happen to the US in the future. The following graph shows the maximum sustainable withdrawal rate by percentage of allocation to stocks for various countries. The graph shows that despite the popularity of the "4% rule", very few countries could sustain a 4% withdrawal rate between 1900 and 2008 (before the crash) regardless of the stock/bond allocation. Even in those few countries, mainly the US and Canada, where it could work reliably, allocation mattered: At 100% stocks no country sustained a 4% withdrawal rate for every 30-year period in the 108 years of the data. Take a country that was not devastated by war in the 20th century like Switzerland or Australia. With a 100% stock allocation, 3% would have been too much for Switzerland but ok for Australia. With a 50/50 stock/bond allocation, 3.5% would have been too much for both countries.

It seems likely that the 21st-century US will do less well than the 20th-century US in terms of maximum sustainable withdrawal rates, given expected stock returns. Notice that except for Spain the countries that at some point failed to support a 2% withdrawal rate were all devasted by WW2. Spain had a civil war in 1936.

Image source: https://www.bogleheads.org/wiki/Trinity_study_update

Image source: https://www.bogleheads.org/wiki/Trinity_study_update

EDIT: @DavePhD asks: If your calculations involve "a 30-year retirement duration", then can't I stick all my money under the matress and use 3.3% percent of the original amount each year, or at least get 0% TIPS [inflation-indexed bonds] and spend a real 3.3% of the original amount a year?

Answer: The mattress strategy, with 2% constant inflation and a 3.33% yearly withdrawal adjusted for inflation of the original amount, will bring you to the end of year 23 and a 2.5% withdrawal rate, to the end of year 29. If you take 3.33% of the original amount out every year without adjusting for inflation, you will have to spend almost half in real terms in year 30 as you did in year 1, which is unacceptable for most people.

The TIPS strategy would work as you describe, assuming that:

- You build a TIPS ladder, with TIPS of different maturities. This means that, if you retire in 2020, you could arrange for 1/30th of your TIPS to mature in 2021, 1/30th in 2022, and so on until 2050. None of this will work if you sell the bonds before they mature, because then you would expose yourself to changes in interest rates. (If rates go up, the value of your bond falls and you will make a loss if you sell, but not if you hold to maturity). By extension, this method will not work with TIPS ETFs. You have to hold the securities yourself and arrange the expected payments (both interest payments and principal repayments) so that you do not have to ever sell the TIPS.

- The real yield is non-negative on purchase (or else you'll have to satisfy yourself with less than 3.33% of the starting amount each year).

- Either a) It is invested in a tax-sheltered account, or b) The after-tax yield is non-negative

- The issuing authority, the US treasury in this case, does not default

- You die on schedule after 30 years.

Point (5) is important. Note that the graph above shows you the maximum withdrawal that always worked for a 30-year period in the past for a given allocation of stocks and bonds. This means that at these maximum withdrawal rates, with 1% of the starting retirement years you would have gotten exactly 30 years of withdrawals. But with the other 99% of the starting years, you would have gotten more years than this, giving you a buffer in case you lived more than 30 years in retirement. With TIPS and 3.33% withdrawals, you have no such buffer, if you don't die before the end of year 30, you will run out of money.

-

2Why do you assume 100% stock allocation? The graph makes it look like Canada, the US and Sweden could all manage the 4% rule at a specific allocation of stocks and bonds.– DuganCommented Oct 8, 2019 at 20:29

-

4That graph is exactly what I wanted. It looks like, if you choose 50% stocks/bonds, the middle line is roughly 3.25%. You can't make assumptions that the next 100 years will be similar to the previous 100 years. On the other hand, I don't think I can trust anyone's forecasts either. Maybe just picking something in the middle is a "good enough" rule. Bernstein says 3% is probably safe, while the middle country on that graph (Sweden) shows 3.25 is probably safe. Seems like "roughly 3%" is a decent guess.– NL3294Commented Oct 8, 2019 at 20:41

-

2@Dugan That was just to show that for the "rule" to work, allocation matters, even though allocation isn't always discussed with the "4% rule". If you just took any allocation, such as 100% stocks, in the 20th century, let alone the 21st, the "4% rule" wasn't guaranteed to work. I agree that for most people it worked in the past for the US and Canada. I don't agree that it worked in Sweden though, because it would have required knowing the best allocation in advance. Most people would not have used a 52/48 stock/bond allocation, which is the only allocation that would have worked without fail.– PertinaxCommented Oct 9, 2019 at 8:58

-

It would be interesting to see Greece in the chart, given that the sock market went to almost 7000 points in early 2000s and now it is at 850, after going below 500 in 2016. Who is to say which is the next stock market that will do that, or if it will even happen globally. Commented Oct 9, 2019 at 11:16

-

3@Pertinax If your calculations involve "a 30-year retirement duration", then can't I stick all my money under the matrass and use 3.3% percent of the original amount each year, or at least get 0% TIPS and spend a real 3.3% of the original amount a year?– DavePhDCommented Oct 9, 2019 at 11:59

The 4% rule was created by looking at hypothetical retirees throughout all of the history of the stock market. 4% was found to always ensure that a retiree never ran out of money for at least 33 years regardless of what period of history you looked at. This includes a retiree going through any of the 30 year periods that intersected the Great Depression, WWI and WWII, Black Monday, and so on. So unless something happens that's worse for the economy than the great depression the 4% rule should be safe.

Source: https://www.investopedia.com/terms/f/four-percent-rule.asp

-

2That's true. But even during the Great Depression, the stock market recouped all losses within a few years, so it really wasn't that bad in the long run. It would be interesting to see how a worldwide diversified stock portfolio would fare under the 4% rule over a long period.– NL3294Commented Oct 8, 2019 at 17:55

-

2Welcome to the forum! Don't forget that despite the crashes, the 20th century produced extraordinary returns for the United States (7% real), both relatively to other countries and relatively to expected returns for the 21st century.– PertinaxCommented Oct 8, 2019 at 19:27

-

1This doesn't answer the question of what happens if the US returns to mean of the rest of the world, this only addresses the US in terms of the history of the US. Commented Oct 9, 2019 at 14:26

I think you could answer this by looking at how the world market does on average compared to the US market. Essentially a comparison of VTSAX to VTWIX. This website will allow you to do exactly that. While VTWIX has a lower growth rate over a 10 year period (8.57% versus VTSAX's 13.09%) it's still higher than the ~7% annualized growth required to make the 4% rule work.

Some other things to consider:

The 4% rule has a lot of assumptions built into it e.g. you're withdrawing at a constant 4% rate, and not adjusting your spending when the market is down. If you're worried about it working as a retirement strategy adjusting your spending to market conditions is probably the best way to make it work better.

The 4% rule refers to how much money you can draw down every year INDEFINITELY. i.e. Your principal will grow at a greater rate than you're withdrawing it at. What this means is that you actually have a lot more money/wiggle room available provided that you're okay diminishing your principal near the end of your life, assuming you're not going to live forever.

This website covers many of the potential issues with the 4% rule.

-

Thanks for that links! I'll see if I can find free datasets of worldwide stock market returns over a long period. It would be very interesting to do the simulations on worldwide averages over say 40 or 50 year spans. If the U.S. reverts to the worldwide average stock market returns, it would make sense for retirees to diversify more into the worldwide markets.– NL3294Commented Oct 8, 2019 at 18:03

-

1@NL3294 even if the US reverts to the worldwide average I'm not convinced it would be better to hold a worldwide stock market tracker because of the higher MER of the fund due to international stock purchases. For a switch to the world stock index you would have to think that the US market is currently overvalued compared to what it should be, or you expect them to become below average in the near future. Two things I don't anticipate happening. If the global market improves the US market will improve too.– DuganCommented Oct 8, 2019 at 18:08