Friend is refinancing a student loan of 155,000 - check the details here or as below.

Total amount now is about 155,000 now. While refinancing with Common Bond , we are getting the following payment terms. We are trying to decide to go between

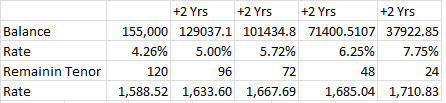

10 year fixed term at 5.72% = $1707.81/month of installment payment or

10 year variable at 4.26% = $1,596.66/month

Variable can go up to 9.99%

Friend is a pharmacist and is planning to pay 2000/month if everything goes ok.

Here are the other terms if any look more attractive.

UPDATE: I learned that with this and some other vendors there is the option to switch between Fixed and Variable as well as there is always that option to refinance again. So would the advice still stand?

UPDATE:

Here is what we ended up doing:

Instead of refinancing both the public and private loans and giving up the benefits on the government loan (Like the loan forgiveness program etc), we decided to consolidate the 13 public loans in to 1 public loan via federal loans itself ( which basically does the weighted average of all the loans) and refinanced the 2 private loans with Sofy. Both at fixed interest rates. For both loans the interest rate is fixed at 5.615% for 10 years (120 payments)

Thus they both are on auto pay qualifying for additional auto pay benefits (0.25%?). So there will only be 2 automatic payments each month which allows to keep an eye on this.

Sofy refinancing allows a few other benefits like unemployment benefits - so the loan can be paused during the unemployment duration, believe they also provide some career assistance, also can refinance it in the future to variable interest rate as well or a reduced fixed rate.

With public loans the benefit is again that one can move on to a different payment plan if hardship arises, the loan forgiveness if the candidate finds a related qualifying job in public service and also I saw another benefit on certain loans that if 12 payments are made on time then there is additional interest reduction.

I believe this gives the best of both the worlds for now. Thanks everyone for your assistance.