The key question is whether this number includes taxes and insurance.

When you get a mortgage in the U.S., the bank wants to be sure that you are paying your property taxes and that you have homeowners insurance. The mortgage is guaranteed by a lien on the house -- if you don't pay, the bank can take your house -- and the bank doesn't want to find out that your house burned down and you didn't bother to get insurance so now they have nothing. So for most mortgages, the bank collects money from the borrower for the taxes and insurance, and then they pay these things. This can also be convenient for the borrower as you are then paying a fixed amount every month rather than being hit with sizeable tax and insurance bills two or three times a year.

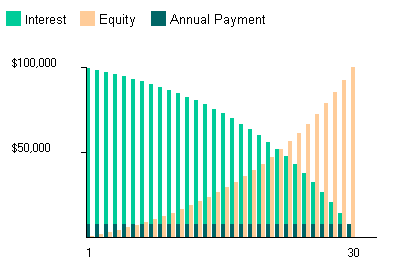

So to run the numbers:

As others point out, mortgage rates in the US today are running 3% to 4%. I just found something that said the average rate today is 3.6%. At that rate, your actual mortgage payment should be about $1,364. Say $1,400 as we're taking approximate numbers.

So if the $2,000 per month does NOT include taxes and insurance, it's a bad deal.

If it does, then not so bad. You don't say where you live. But in my home town, property taxes on a $300,000 house would be about $4,500 per year. Insurance is probably another $1000 a year. And if you have to get PMI, add another 1/2% to 3/4%, or $1500 to $2250 per year. Add those up and divide by 12 and you get about $600. Note my numbers here are all highly approximate, will vary widely depending on where the house is, so this is just a general ballpark. $1400 + $600 = $2000, just what you were quoted.

So if the number is PITI -- principle, interest, taxes, and insurance -- it's about what I'd expect.