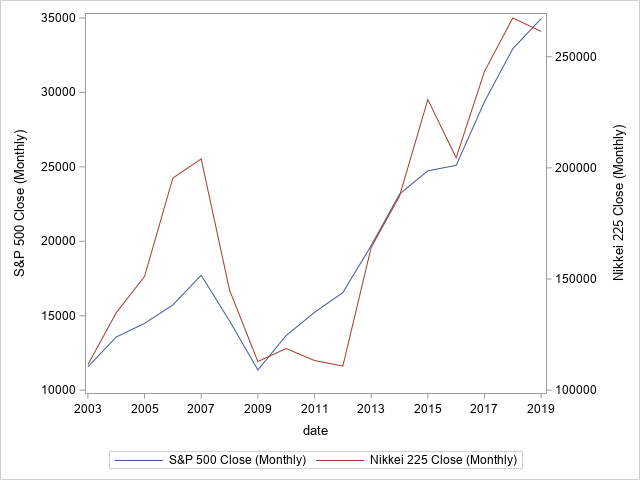

The Japanese economy has had a unique history, with a huge bubble in the 1980s and a long unwinding afterward.

I don't see why that would result in a market that appears to have brief periods of growth. If anything, I'd expect their recent economic history to produce a market that goes straight down, rather than inconsistently hovering back up.

Apart from specifics of Japan, this confusion can be addressed via general principles of markets. No market can literally head "straight down" for an extended period, because if there were such a predictable pattern, intelligent traders would "front-run" by selling and shorting so much that the expected decline would happen "all at once".

According to the efficient market hypothesis, the market discounts all available information and its movements are driven only by new information (the deviation from previous expectations). The market is inherently two-sided; at any given time, there are reasonable bets for it to go up as well as down, or it would not be at the price it is.

Once a piece of bad news becomes known, the corresponding market decline is immediate rather than gradual. At that point, the projections are "baked in", and any subsequent updates that raise a bit of hope ("slightly less bad") will cause a market rally. Market movements always look something like a random walk (Brownian motion) because prices would not be equilibrium if they did not have the potential to go up as well as down.

In the case of Japan, you see many rallies and declines over the years as recovery hopes waxed and waned. Overall, the trend continued down as economic projections met with disappointment more often than not.