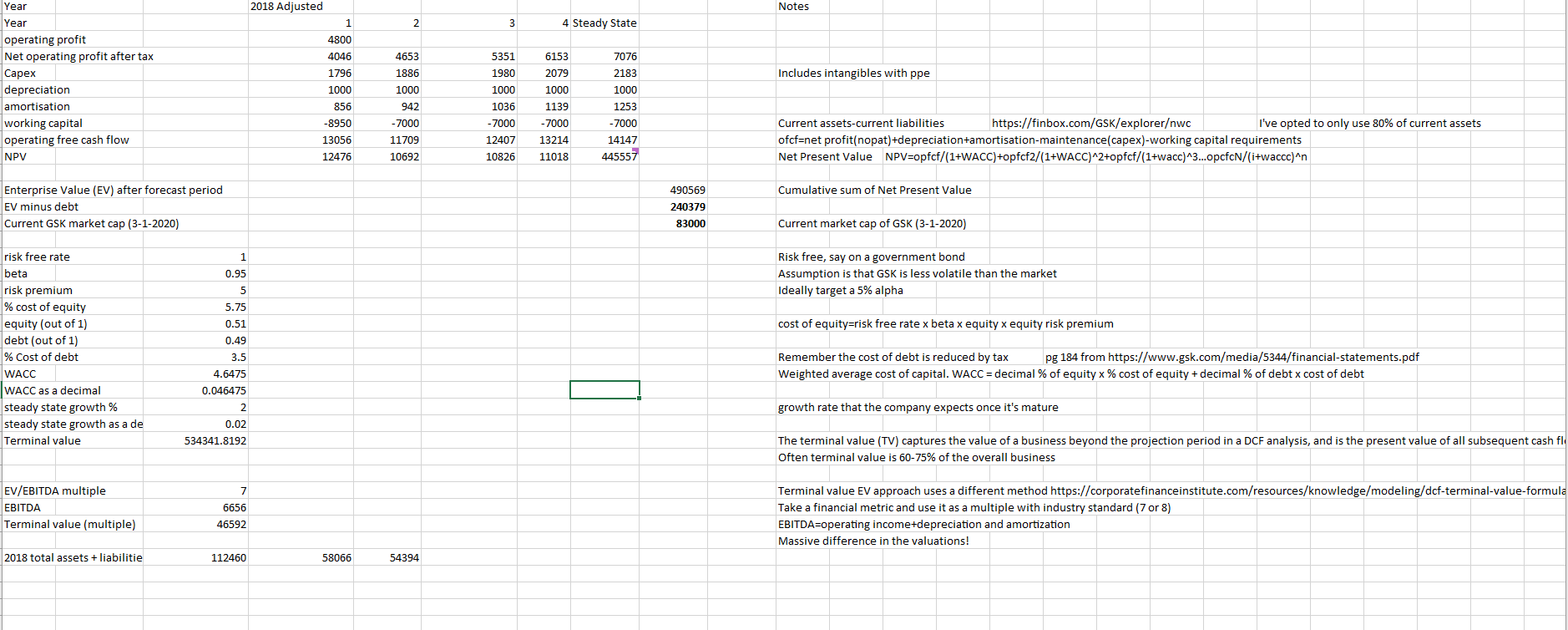

After reading "How to Analyse Companies and Value Shares" by the FT, I've made my own Excel DCF model for GlaxoSmithKline. The problem is that it gives huge variations in Enterprise Value if I only slightly adjust the model inputs. For example:

If I use a modest steady state growth rate, e.g. 5.5% I get a negative Enterprise Value (EV). I don't believe GSK will be worth a minus investment in several years to come.

- If I use a very low steady state growth rate,say 2% I suddenly get an EV of £240 billion!

In other words, if I use a lower growth rate, I get a higher valuation (as the Weighted Average Cost of Capital is now higher than the growth rate).

I'd be grateful if someone could take a look at the model and provide some guidance on how to DCF properly, because at the moment, given the variations, the valuations just seem wrong. I've double checked the calculation formulas which seem to be correct.

Advice appreciated.

Thanks