Debt funds are exposed to fixed income risks, which overlap with but are not the same as equity risks. Equity, for example, falls during every recession. Debt may or may not.

The main risks you face in fixed income assets are:

- Inflation risk. If inflation ends up being higher than expected, the price of your fixed-income assets will likely fall because the payments made will buy fewer goods and services than expected. This is mitigated by buying funds or assets with a short horizon.

- Real interest rate risk. If interest rates rise (above expectations) after your purchase of the fixed income securities, the price of your securities or fund will fall and you will lose money, when compared with not having made the investment. If you sell early, this loss will be obvious. If you hold to maturity, then the loss is relative to what you would have gotten in other assets. This risk is mitigated by buying shorter-term debt.

- Default risk. The assets you buy (or your fund does) don't pay out all that they promised to. This it mitigated by buying higher quality debt and also shorter-term. This type of debt also tends to have a lower yield.

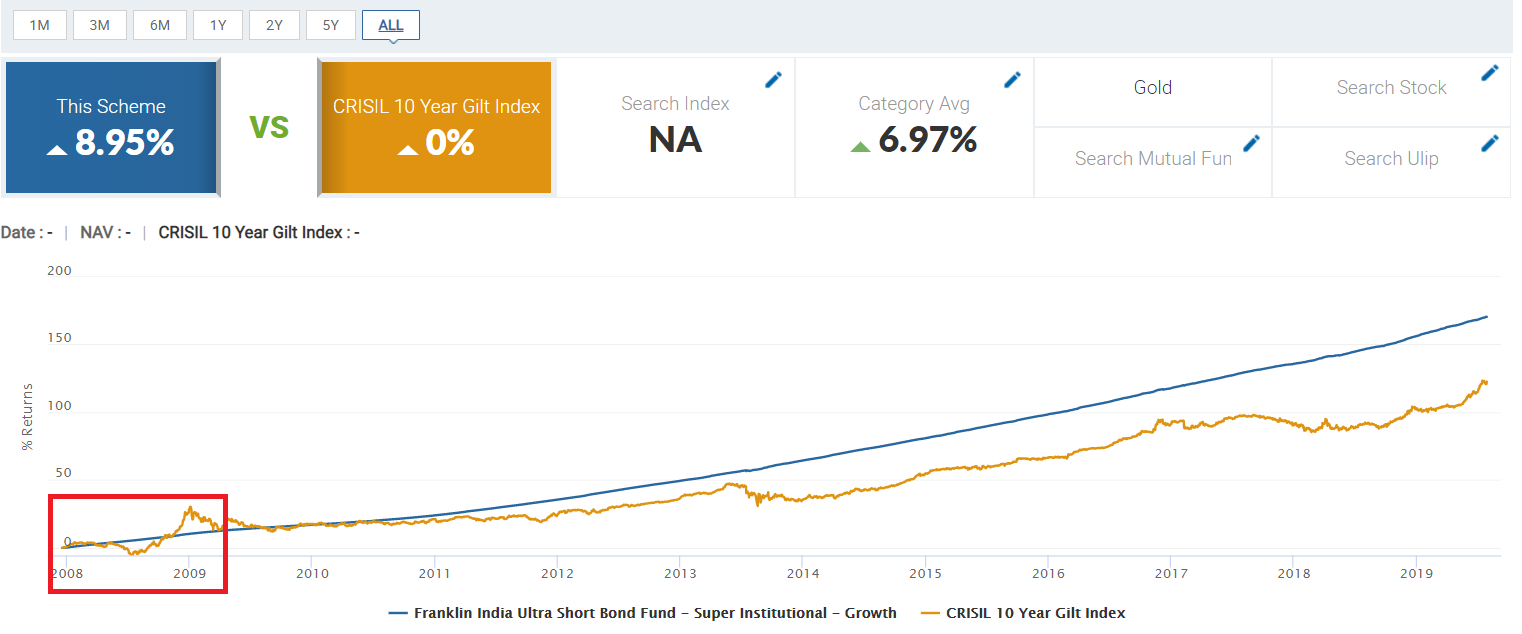

Your analysis mostly looks at recessions. Recessions are certainly associated with losses in low quality (high yield) debt, but not so much with high quality debt. In fact, during recessions, people tend to sell riskier stuff and buy high quality debt so you may actually make money as the prices of those bonds rise. If recession risk is your top concern, then buying high-rated debt (triple A or certain government debt) is a good strategy.

Perhaps the usual risks people talk about in fixed income are inflation and real interest rate risk. Long duration bonds are associated with higher volatility of their prices. To avoid these risks, the primary strategy is to buy shorter-maturity securities.

A fund buying short-term high-quality securities tries to avoid all three risks and will very seldom lose money; when it does, it won't lose much. On the other hand, it will never make much money either. This is analogous to an equity portfolio that seeks to minimize its market exposure: it won't lose as much during a recession, but you won't expect it to make much during good times either.

TLDR: funds with high-quality debt are recession-proof but not protected against inflation or rising interest rates, which may or may not happen during a recession (mostly not). Short-term debt is robust to inflation and rising interest rates. Funds that have short-term and high-quality debt are pretty much as safe as investable assets get.