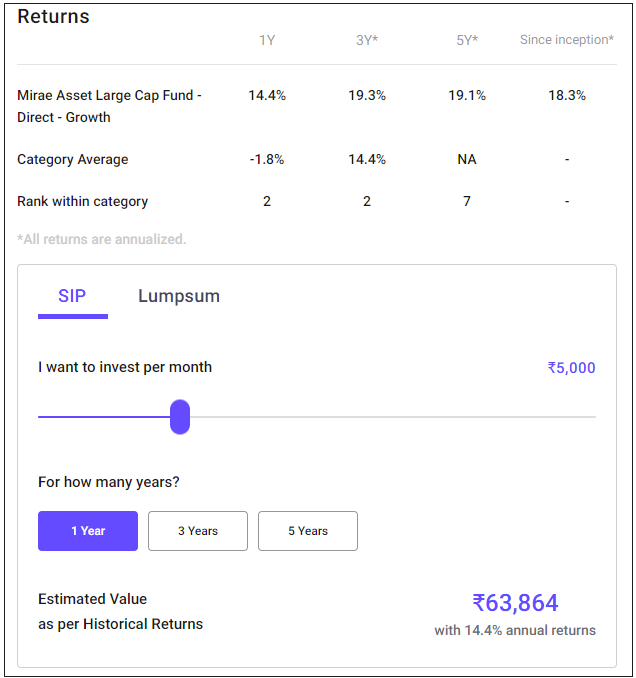

I couldn't see the fund in your screenshot, but here is the one from the web link.

The one-year return can be calculated like so.

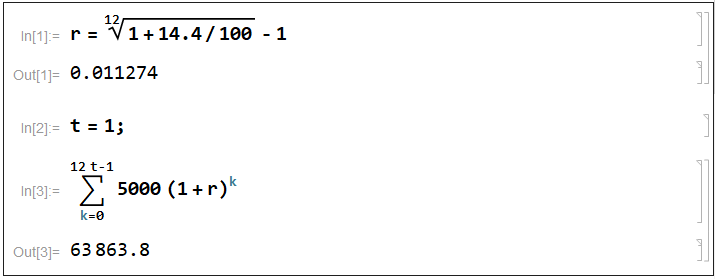

Also using a formula

a = d ((1 + r)^n - 1)/r

where

a is the future amount

d is the monthly payment (paid at month-end)

n is the number of months

r is the monthly interest rate

The annual interest rate is 14.4%

r = (1 + 14.4/100)^(1/12) - 1 = 0.011274

n = 12

d = 5000

a = d ((1 + r)^n - 1)/r = 63863.84

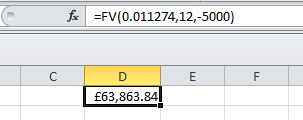

The same in Excel

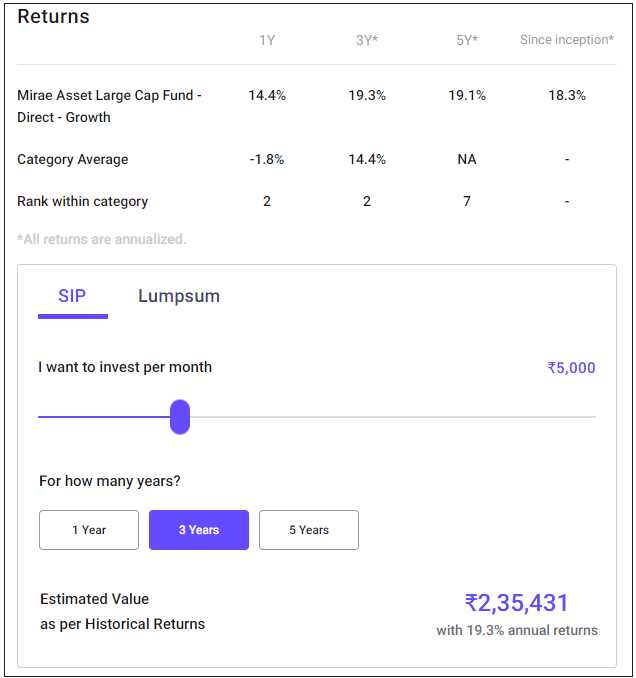

The 3 year result is a little out, presumably some rounding inaccuracy

r = (1 + 19.3/100)^(1/12) - 1 = 0.0148146

n = 36

d = 5000

a = d ((1 + r)^n - 1)/r = 235556.95

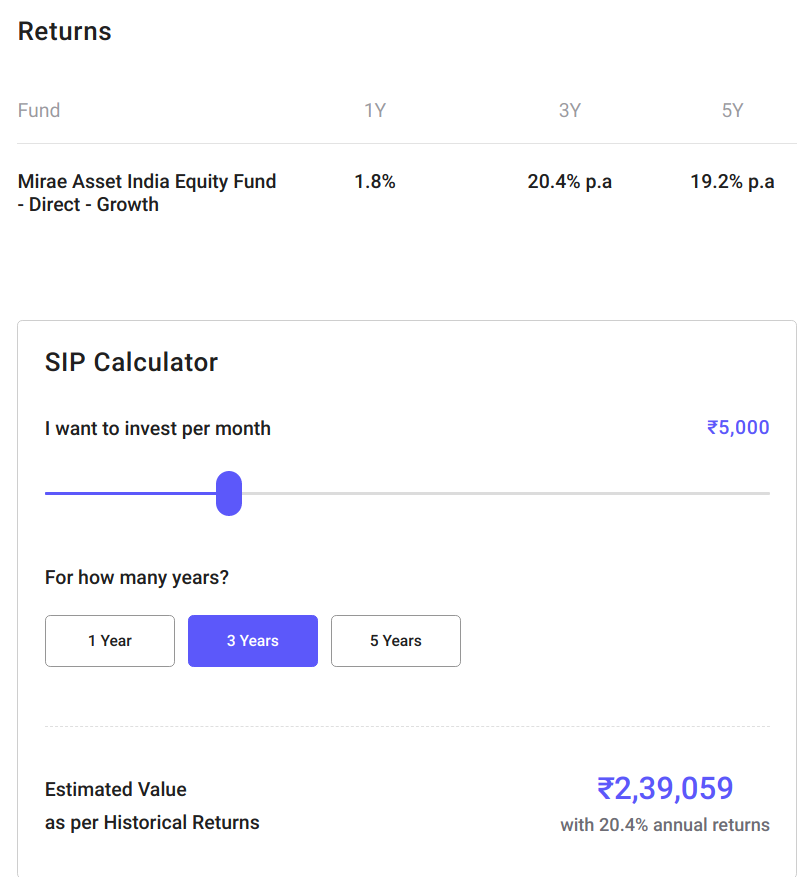

A 3 year annualised return of 19.26% obtains the website figure, shown below.

r = (1 + 19.26/100)^(1/12) - 1 = 0.0147862

n = 36

d = 5000

a = d ((1 + r)^n - 1)/r = 235431.40

I would guess the interest rate in the calculations is 19.26% but the website shows the figure rounded to one decimal place, as 19.3%.

{kind=link}

{kind=link}

{kind=link}

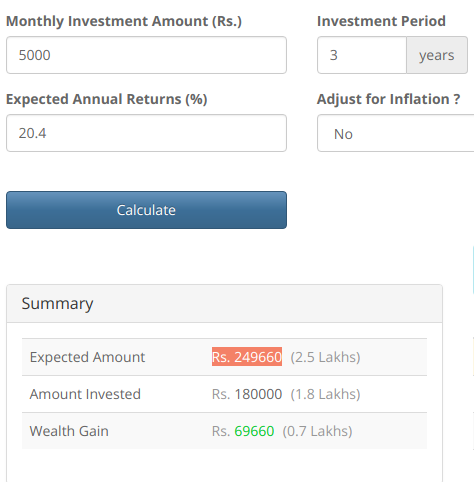

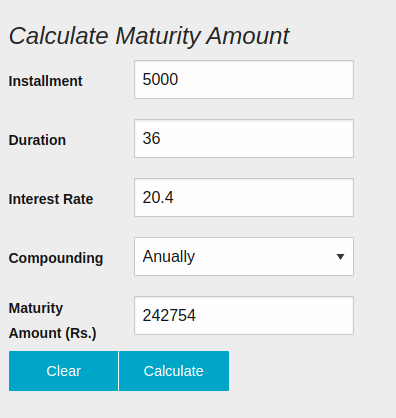

=FV((1+20.41/100)^(1/12)-1,36,-5000)produces 239059. All explained in my answer.=FV(20.4/100/12,36,-5000,0,1)producing 249660. The main differences are that the interest rate here is nominal compounded monthly rather than effective annual rate, and the payments are at month-start rather than month-end. Presumably the Mirae calculator uses month-end payments because the lump sum calculates from month-start and they don't want a SIP payment at the same time as the lump sum, but it means the last SIP payment accrues no interest.=FV((1+20.4/100)^(1/12)-1,36,-5000,0,1)producing 242754.