For starters, why bank executives and marketing companies make decisions is anyone's guess. Clearly the folks making these decisions think competing on points is a more effective method of customer acquisition.

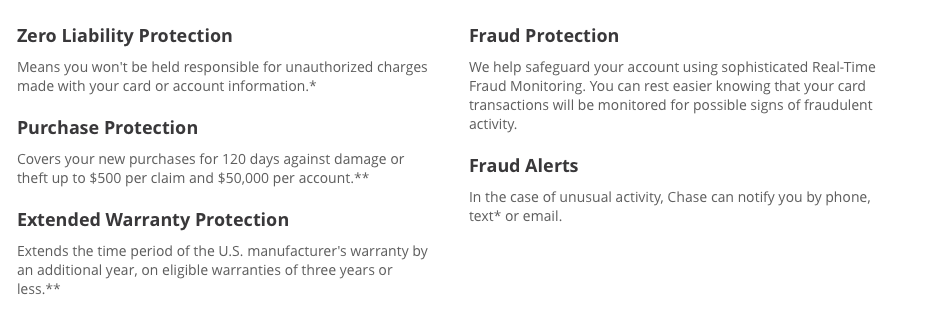

I'm not versed enough to understand whether it's the interchange network (Visa/Mastercard) underwriting the insurance or if it's the bank. If it's the interchange network it's not a point of differentiation, if it's the bank it's a cost center.

Getting a customer and keeping a customer are different. Sign up and I'll give you $200 is a good method of acquiring a new customer; certainly better than sign up and maybe in the future you might buy something just before a price decrease and the merchant won't price match so we'll price match it for you. If you were closing your account "But remember that we offer extended warranty on anything you purchase, are you sure you want to close the account and give up that coverage?" might be effective to keep you.

There was a time that the major credit card benefits were all purchase insurance related. They were paid for by your annual fees. For American Express these lines of coverage are literally underwritten by a subsidiary insurer. Really there was a time that the only benefit to a credit card was the simple fact that you didn't need to carry the cash. Competition grew the array of benefits. To some extent the purchase protection benefits are just a relic of the days before cash-back and are actually quietly being dropped from some cards particularly the non-flagship no-annual fee cards that have to compete with points now too.

Over time laws have expanded and imposed some of these things on merchants anyway, like mandatory returns within X days. Once a merchant has a legal obligation to take an item back it only makes sense to price match it within the X days so at least they don't have to restock the item and this merchant requirement really dilutes the value of purchase price protection offered by your credit card.

Personally, one of the selling points for me on my main card was primary rental car insurance. A lot of cards have rental car coverage, but it's secondary to your personal car insurance, this one is primary.