Timeline for Stock market long term risks

Current License: CC BY-SA 3.0

24 events

| when toggle format | what | by | license | comment | |

|---|---|---|---|---|---|

| Feb 29 at 10:44 | comment | added | sidgate | Hang Seng Index is now at the same level as it was 20 years before. "Long term" is different for different person. If someone was investing with SIP for retirement, he would be at loss right now. So no, historical numbers don't mean anything | |

| Jun 4, 2023 at 19:31 | comment | added | ispiro |

I revisited some of my old questions, and regarding your statement that and each down year was completely (or mostly) recovered within 2 years, followed by multiple years of growth - I'll point out that an answer to a different question of mine by Bob Baerker states that around the year 2000 it was actually around a decade to recover. Are your answer and his contradicting, or am I missing something here?

|

|

| Sep 6, 2018 at 4:10 | comment | added | C.J. Jackson | @Beanluc, the problem is not so much with one index itself, but rather different indices. Looking at 90 years of performance for the S&P 500 is a practice in survivorship bias because 90 years ago, nobody knew the US was going to be where it is today. If you had invested in the S&P 500 of another nation (like Argentina which was on-par with the US), you would've not had anywhere close to the growth you experienced with the US. | |

| Sep 5, 2018 at 23:51 | comment | added | Beanluc | @C.J.Jackson Does the index really exhibit a survivorship bias? Does its value not reflect the losses from those companies which died, disappeared or got de-listed before being replaced with healthier companies? Last question: As an index investor, should you not expect to keep up with the index and its survivors, or do you believe that investors in index-fund products cannot in fact keep up with the "bias" as the contents of the funds are revised to continue matching the contents of the index itself? | |

| Apr 25, 2018 at 20:50 | comment | added | Zulan | "each down year was completely (or mostly) recovered within 2 years" - really? The chart I am looking at, it seems that it took until 2015 to recover to the level of 2000. | |

| Apr 24, 2018 at 22:02 | comment | added | user2652379 | @Ant You are right. But diversification is a methodology. It can be applied to other assets like bonds. I like diversification, but I'm looking for stock market-based reasoning. | |

| Apr 24, 2018 at 18:10 | comment | added | Aleksandr Dubinsky | If the structure of the economy changes in a dramatic way such that there is much more competition and much lower profits, the stock market will crash in an unrecoverable way. The gains of the stock market over the past decades parallels the rich getting richer in America. That could change (without necessarily involving a full-blown communist revolution). | |

| Apr 24, 2018 at 17:05 | comment | added | jamesqf | @gerrit: In addition to those who do not have money to invest, there are a large number of people who do have the money, but prefer to spend it on other things. | |

| Apr 24, 2018 at 16:39 | comment | added | C.J. Jackson | The problem I have with 90 years of S&P500 return is the big survivorship bias. US had done the best economically in the past 100 years. 100 years ago, US and Argentina were at similar level economically. You think Nikkei investors after 1990 has recovered their money? This is not even to mention other types of risks, like millionaires in China in 1948, or rich people in pre-revolution Cuba. | |

| Apr 24, 2018 at 13:22 | comment | added | D Stanley | @phresnel The 5 years I quoted was including inflation (the dollar depreciated over that time) and dividends (which were still being paid throughout the 1930s) | |

| Apr 24, 2018 at 13:21 | comment | added | D Stanley | @Cloud Do some research here on borrowing to invest - these returns are average and can swing from +40% to -30% in one year. A mortgage is fixed, so financing risky returns with a fixed interest payment is not comparable. | |

| Apr 24, 2018 at 12:43 | comment | added | Seth R | @Cloud, people that invest well generally do become rich. At least rich enough that they can quit their jobs and live off their investments. But it does take a while. Most people don't get there until they are about 65. | |

| Apr 24, 2018 at 12:21 | comment | added | Cloud | @gerrit Well, actually based on these returns even with a mortgage, you should invest at the same time as it provides better returns than paying the mortgage off quicker... | |

| Apr 24, 2018 at 12:12 | comment | added | gerrit | @Cloud Because the large majority of people do not have any money spare to invest at all. The large majority of people have more debts (mortgage) than savings or investments. Anyone who owns a house debt-free and has money left to save or invest, is relatively rich (but having 10k to invest in an index fund does not make one millionaire rich). | |

| Apr 24, 2018 at 11:48 | vote | accept | ispiro | ||

| Apr 24, 2018 at 11:23 | comment | added | Cloud | Based on this answer, why isn't everyone rich? If everyone invested in SP500 then everyone would be rich.. | |

| Apr 24, 2018 at 11:05 | comment | added | Ant | @user2652379 If you have a well diversified portfolio (say you buy the SP500) and there is a year where you have a 99% market downturn, then you really shouldn't worry about your stock performance. A 99% loss in value in the 500 biggest companies in the country means that the economy has essentially collapsed and your main problem has just become to find food and avoid being killed in the ensuing rampage of violence. | |

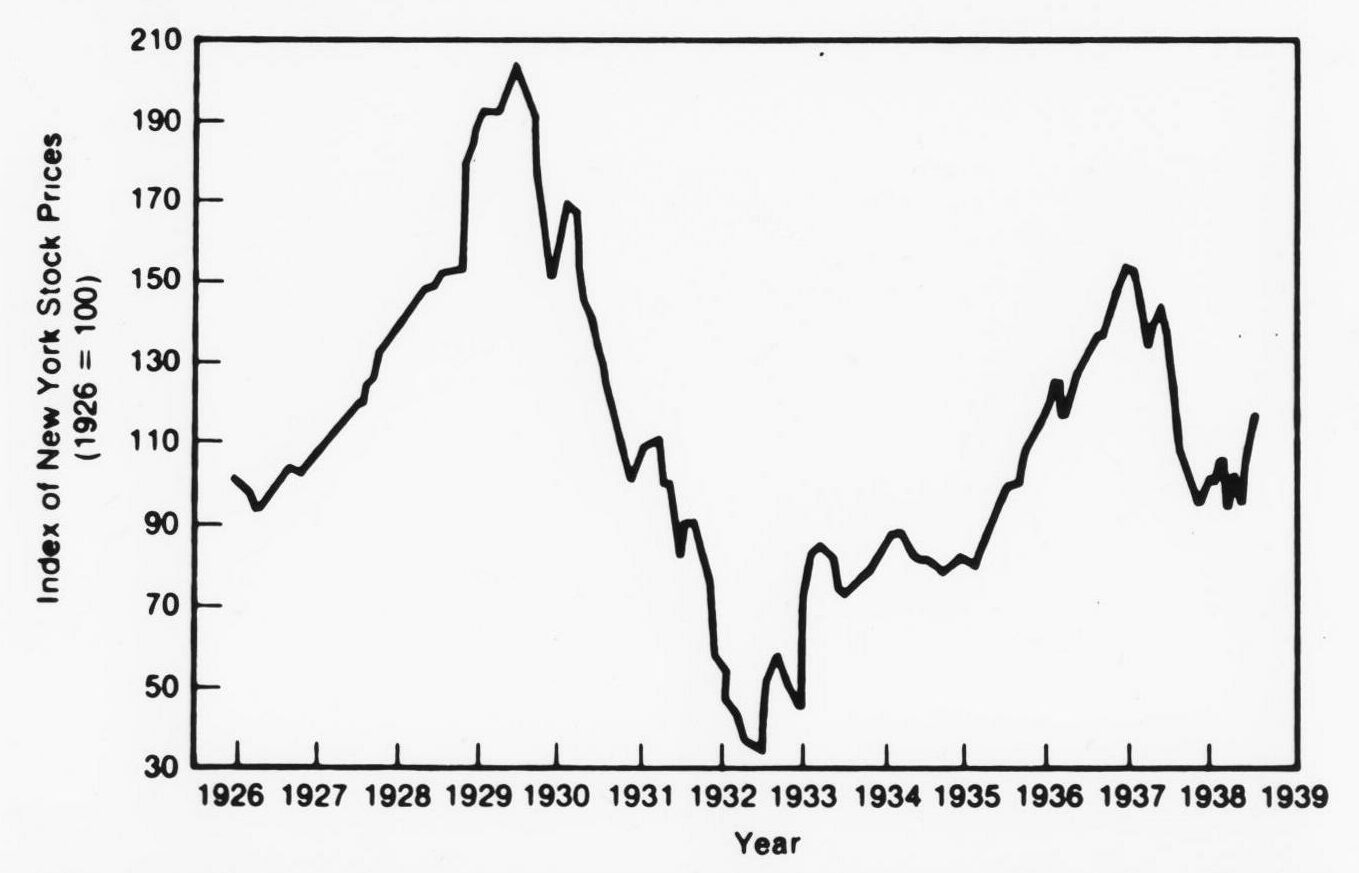

| Apr 24, 2018 at 9:51 | comment | added | phresnel | Two years recovery may not be incorrect, but depends on standpoint. If you invested everything in 1928, recovery would be more like in 1936. "Just 8 years" may translate to age 65-73 years, so that instead of 13 happy years as a German Average Male, I'd have just 5 happy crippled years (see upload.wikimedia.org/wikipedia/commons/3/38/Stocks29.jpg). I understand people prefer to decline the possibility of dying, especially when it comes to their own death, and therefore underestimate how much time a few years actually can be. But they really shouldn't. | |

| Apr 24, 2018 at 5:09 | comment | added | user2652379 | So we basically believe in market history? I hoped for the better reasons, but I can't find any... | |

| Apr 23, 2018 at 15:13 | comment | added | Seth R | This of course assumes your portfolio is well-diversified across many categories of stock. Your experience would be very different if you had everything invested in, say, 8-track tapes and film cameras. | |

| Apr 23, 2018 at 13:49 | history | edited | D Stanley | CC BY-SA 3.0 |

added 5 characters in body

|

| Apr 23, 2018 at 13:41 | comment | added | D Stanley | I did not say that it would not pay to invest. It just took longer to recover in that era, which had more issues than just stock losses. Over 60 years, the effects of compounding returns is unbelievable. | |

| Apr 23, 2018 at 13:35 | comment | added | ispiro | Thanks. But I guess I worded my question wrong. I didn't mean everything as in 100%. I was referring to something like the great depression. I didn't quite understand your statements about it. At first it seems you're stating that even then, the loss was limited, and later it seems you're saying that if such a case occurred again (between the investor's 20th and 80th birthday in my question), it wouldn't pay to invest. Where's my mistake? | |

| Apr 23, 2018 at 13:30 | history | answered | D Stanley | CC BY-SA 3.0 |

{kind=link}