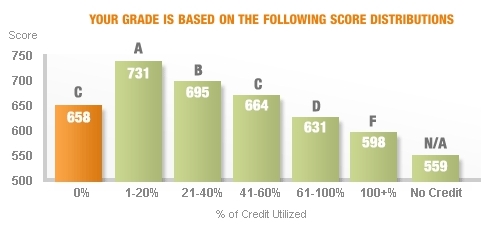

This chart above is taken from a Credit Karma snapshot I used in an article titled Too Little Debt? 30% of your score is based on utilization and this portion is scored as the chart indicates. A 61-100% utilization should really be avoided, but once paid, your score does bounce back, real time.

2018 update - Note that not all cards report your statement balance. Since posting this answer, 7 years ago, one of my cards changed banks. Now, the end of month balance is reported as compared to the fact the statement is cut on the 15th of the month. To 'game the system' and optimize utilization, I need to make a payment by the 30th/31st including those charges made since the statement was cut. In effect, I need to give up 2 weeks of float on this money. With near zero interest rates, not a big deal. And of course, the last 10-20 points on my FICO score make little difference even when applying for credit, as my score is above 800.