For example, if the portfolio is financed with 50% margin, does it affect the portfolio variance?

2

-

Just out of curiosity (as I am very new to the community), should this (and some other similar questions) go instead to the Quantitative Finance SE? Or would that site discourage such questions?– ApoorvCommented Jun 11, 2011 at 16:39

-

If I were you, I would accept Havoc's answer. It is much more detailed than mine and in my corrected opinion better answers the question from the investor's viewpoint (which I assume is your viewpoint as well).– ApoorvCommented Jun 11, 2011 at 19:48

Add a comment

|

3 Answers

Yes, more leverage increases the variance of your individual portfolio (variance of your personal net worth). The simple way to think about it is that if you only own only 50% of your risky assets, then you can own twice as many risky assets. That means they will move around twice as much (in absolute terms). Expected returns and risk (if risk is variance) both go up. If you lend rather than borrow, then you might have only half your net worth in risky assets, and then your expected returns and variation in returns will go down.

Note, the practice of using leverage differs from portfolio theory in a couple important ways.

- There's a threshold or cliff danger, which is when the broker makes you force-sell your assets, or you have to declare bankruptcy, or whatever. Then you are just stuck with a loss and you can't hold and wait for prices to go back up. Leverage thus allows you to lose 100% of your assets, permanently. Another way to put it is that margin calls can create a cash crisis or lack of liquidity, destroying you.

- the interest rate charged by brokerages is pretty far above the risk-free rate, if you're just an average joe individual. This lowers expected return for a given risk, so the CML bends at the point where leverage begins and leverage isn't as useful as it would be. http://www.investing-in-mutual-funds.com/asset-allocation.html has an illustration of this.

Financing a portfolio with debt (on margin) leads to higher variance. That's the WHOLE POINT. Let's say it's 50-50.

On the downside, with 100% equity, you can never lose more than your whole equity. But if you have assets of 100, of which 50% is equity and 50% is debt, your losses can be greater than 50%, which is to say more than the value of your equity.

The reverse is true. You can make money at TWICE the rate if the market goes up. But "you pay your money and you take your chances" (Punch, 1846).

-

@Monster Truck, I think you are talking about variance of the market portfolio. But the "lens" changes the variance of the actual investor's portfolio, which I would say is the question.– Havoc PCommented Jun 11, 2011 at 19:11

Variance of a single asset is defined as follows:

σ2 = Σi(Xi - μ)2

where Xi's represent all the possible final market values of your asset and μ represents the mean of all such market values.

The portfolio's variance is defined as

σp2 = Σiwi2σi2

where, σp is the portfolio's variance, and wi stands for the weight of the ith asset.

Now, if you include the borrowing in your portfolio, that would classify as technically shorting at the borrowing rate. Thus, this weight would (by the virtue of being negative) increase all other weights. Moreover, the variance of this is likely to be zero (assuming fixed borrowing rates). Thus, weights of risky assets rise and the investor's portfolio's variance will go up.

Also see, CML at wikipedia.

-

I'm not sure you have this right. I would say: that equation for variance is how you would compute a variance post-facto after knowing the data points, with a given portfolio. It isn't relevant here. Borrowing or lending does not change the slope of the CML, it's moving you along the CML. As you move along the CML, your expected returns and your variance (or SD) move proportionally together. So all else equal, leverage increases variance (because you own more risky assets).– Havoc PCommented Jun 11, 2011 at 19:00

-

Hi @Havoc. Borrowing/lending will change the slope of the CML if the borrowing rate is different from the risk free rate (which almost always is the case). Leverage does not increase variance --in fact in the plot I have for CML, variance is the X-axis. Second, how does being leveraged make you own more risky assets? What if I borrow $100 from you to invest in a $100 T-bill? I still have zero market risk (discounting inflation) but I am of course leveraged. I will need to pay you back at whatever rate you lend me but that does not increase the risk because the payment is fixed.– ApoorvCommented Jun 11, 2011 at 19:12

-

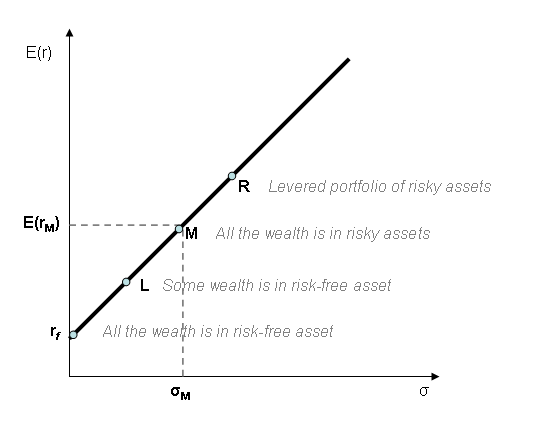

i.e. the issue is not the variance of the market portfolio M, the issue is how the variance experienced by the investor changes as they choose less (L) or more (R) leverage, in that graph. That variance changes.– Havoc PCommented Jun 11, 2011 at 19:12

-

@Monster Truck I would say "leveraged" means your net ownership of the risk-free asset is negative, i.e. you are borrowing money on balance. Just having a loan doesn't mean you are overall leveraged. I agree that a borrowing rate different from risk-free changes CML slope, in fact I just mentioned the same in my answer, but whatever its slope, the variance (on X axis) is higher as you increase leverage. That's the whole point of the line, that as you move along it you get more variance and higher returns.– Havoc PCommented Jun 11, 2011 at 19:17

-

Here is my understanding: the CML shows a range of portfolios with varying leverage; the portfolios each have a different variance (X axis) and expected return (Y axis). The portfolios differ only in degree of leverage. The point of the line is that 1) higher returns and higher risk go hand-in-hand and 2) the "correct" way to increase/decrease both risk and returns is to vary your leverage (positive or negative), rather than deviate from the market portfolio on another dimension, such as changing the weighting of risky assets vs. the market weighting.– Havoc PCommented Jun 11, 2011 at 19:28